Dubai Residential Market June 2026 recorded 5,263 freehold apartment transactions worth AED 8.10 billion during June 1–15, 2026. This data brief examines off-plan activity, buyer preferences, affordability trends, active projects, leading locations and the concentration patterns shaping Dubai’s residential market.

Nearly half of all apartment transactions were concentrated within just five areas, highlighting how market activity is becoming increasingly focused around a small number of locations.”

Dubai Residential Market Brief | June 1–15, 2026

Market Overview

| Metric | Value |

| Transactions | 5,263 |

| Sales Value | AED 8.10 Bn |

| Average Ticket Size | AED 1.54 Mn |

| Median Ticket Size | AED 1.09 Mn |

| Average Price | AED 1,848 psf |

| Median Price | AED 1,720 psf |

| Median Unit Size | 724 sq ft |

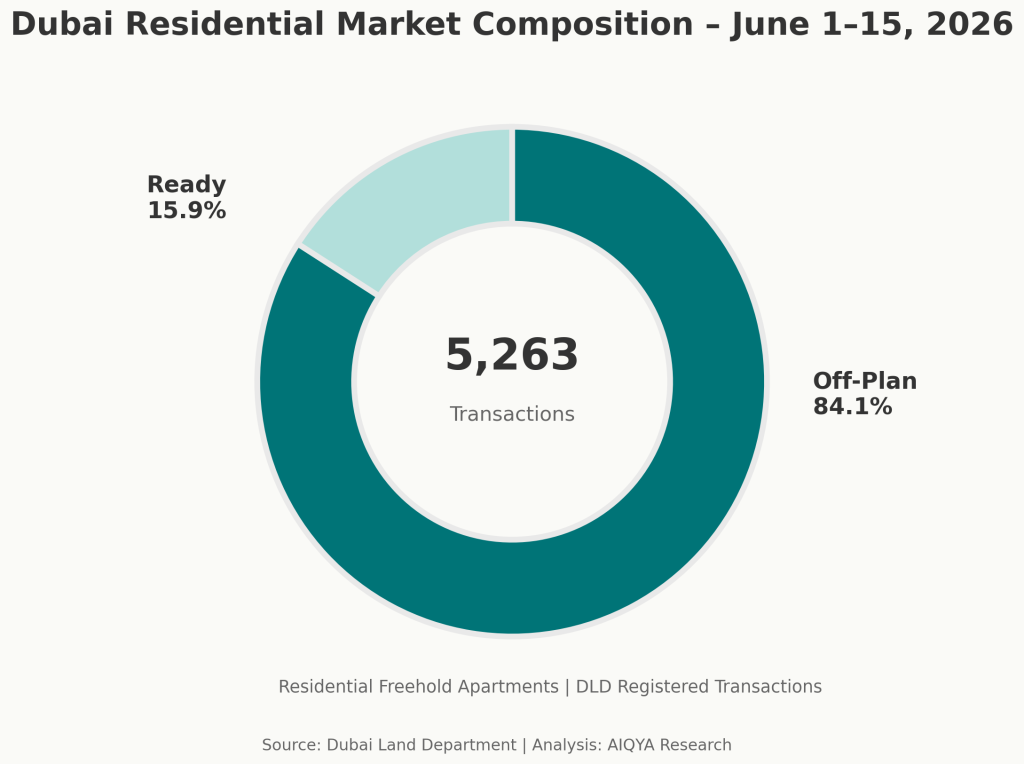

| Off-Plan Share | 84.1% |

Residential Freehold Apartments | DLD Registered Transactions | June 1–15, 2026

Dubai’s residential apartment market remained firmly launch-led during the first half of June 2026. Off-plan transactions accounted for more than 84% of all registered activity, while compact homes continued to dominate buyer demand. The data points to continued concentration, with a relatively small number of locations, projects and launch platforms accounting for a significant share of market activity.

This snapshot provides a data-first overview of transaction activity before a longer-form AIQYA market interpretation report.

Executive Summary

- 5,263 residential apartment transactions worth AED 8.10 billion were registered during June 1–15, 2026.

- Off-plan sales accounted for 84.1% of all activity, up from 80.2% in May.

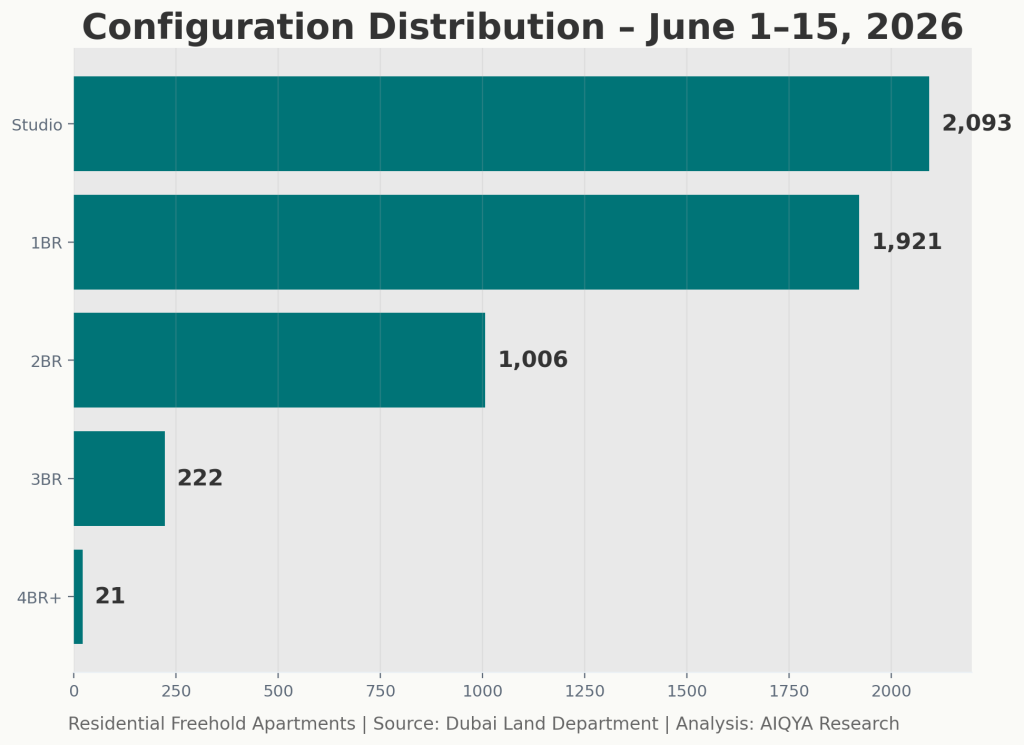

- Studios and one-bedroom apartments represented 76.3% of all transactions.

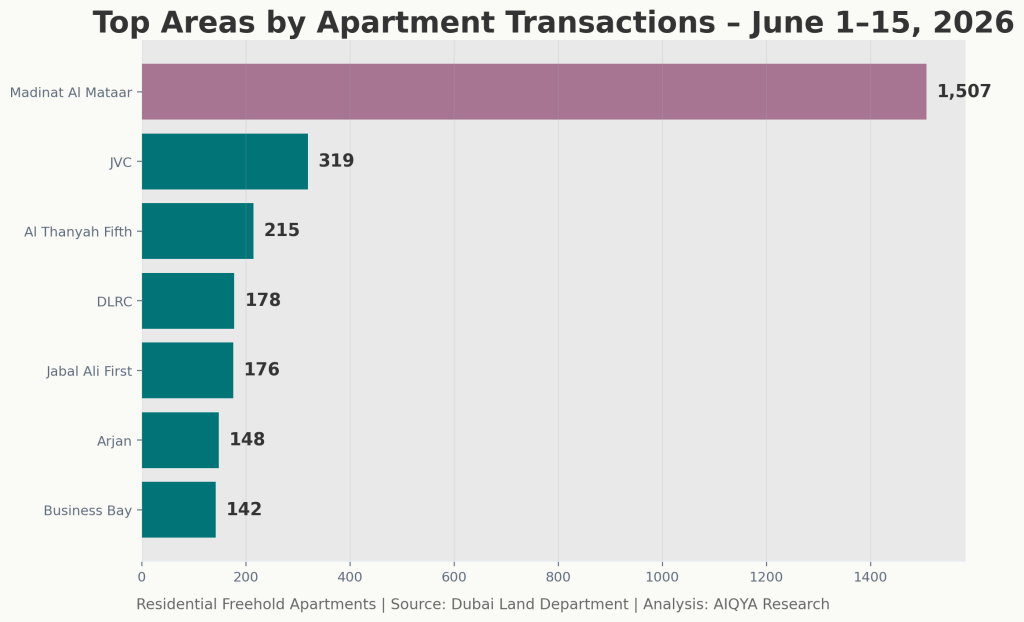

- Madinat Al Mataar accounted for 1,507 transactions, representing approximately 28.6% of all apartment sales recorded during the period.

- Azizi-branded projects represented approximately one-third of identified activity based on project naming patterns.

- Luxury homes above AED 5 million accounted for just 2.4% of transactions but generated more than AED 1.2 billion in sales value.

Market Concentration Snapshot

| Metric | Value |

| Top 5 Areas Share | 45.5% |

| Top 10 Areas Share | 58.0% |

| Top 20 Areas Share | 74.2% |

| Largest Project Share | 12.9% |

| Largest Brand Share* | 33.3% |

*Brand share is estimated from project naming patterns and should not be interpreted as statutory developer market share.

Dubai Residential Market Composition June 1-15, 2026

Off-Plan vs Ready Market

| Segment | Transactions | Share | Median Price |

| Off-Plan | 4,425 | 84.1% | AED 1,748 psf |

| Ready | 838 | 15.9% | AED 1,374 psf |

The first half of June reinforced Dubai’s dependence on the primary market. More than four out of every five apartment transactions originated from off-plan inventory, highlighting the continued influence of developer launches on transaction volumes.

Compact homes remain Dubai’s liquidity engine, while developer launches continue to act as the primary catalyst for transaction activity.

Configuration Distribution June 1-15, 2026

Configuration Distribution

| Configuration | Transactions | Share | Median Ticket | Median Price |

| Studio | 2,093 | 39.8% | AED 655,000 | AED 1,759 psf |

| 1BR | 1,921 | 36.5% | AED 1.25 Mn | AED 1,642 psf |

| 2BR | 1,006 | 19.1% | AED 2.14 Mn | AED 1,691 psf |

| 3BR | 222 | 4.2% | AED 4.16 Mn | AED 2,232 psf |

| 4BR+ | 21 | 0.4% | AED 10.30 Mn | — |

Studios and one-bedroom apartments together accounted for 76.3% of all transactions, confirming that compact homes remain the liquidity engine of Dubai’s residential market.

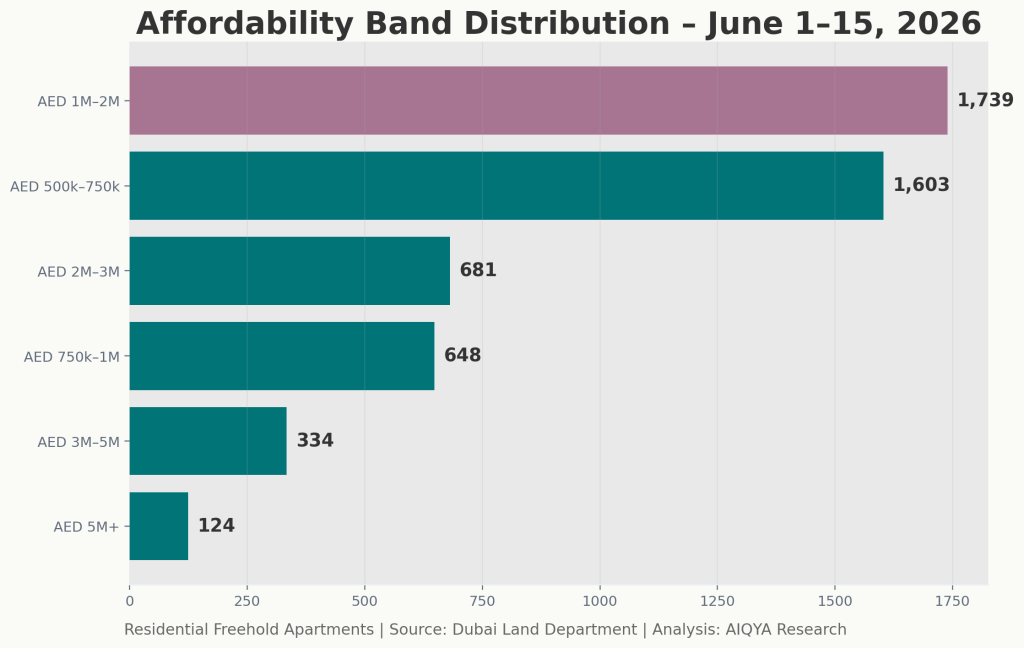

Ticket Band Distribution

| Ticket Size Band | Transactions | Share |

| Under AED 500k | 134 | 2.5% |

| AED 500k–750k | 1,603 | 30.5% |

| AED 750k–1M | 648 | 12.3% |

| AED 1M–2M | 1,739 | 33.0% |

| AED 2M–3M | 681 | 12.9% |

| AED 3M–5M | 334 | 6.3% |

| AED 5M–10M | 93 | 1.8% |

| AED 10M+ | 31 | 0.6% |

The AED 1M–2M segment remained the largest affordability bracket, accounting for one-third of all transactions. Together, homes priced below AED 2 million accounted for approximately 78% of all transactions, reinforcing the market’s continued affordability focus.

Unit Size Trends

| Unit Size Band | Transactions | Share |

| Under 400 sq ft | 919 | 17.5% |

| 400–600 sq ft | 1,082 | 20.6% |

| 600–900 sq ft | 1,777 | 33.8% |

| 900–1,200 sq ft | 594 | 11.3% |

| 1,200–1,600 sq ft | 563 | 10.7% |

| 1,600–2,500 sq ft | 260 | 4.9% |

| 2,500+ sq ft | 68 | 1.3% |

The centre of gravity remained between 400 and 900 sq ft, mirroring the continued dominance of studios and one-bedroom apartments.

Corridor Lens

Dubai South Corridor

Madinat Al Mataar and Jabal Ali First continued to dominate transaction activity, supported by large-scale off-plan launches and investor-oriented inventory. This corridor represented the strongest concentration of residential activity during the first half of June.

Dubailand Corridor

DLRC, City of Arabia and surrounding affordability-led locations continued to attract value-conscious buyers seeking lower entry prices.

Urban Core Corridor

Business Bay and Al Thanyah Fifth recorded lower transaction volumes than Dubai South but significantly higher ticket sizes and pricing levels, reflecting sustained demand for centrally located urban apartments.

Top Areas by Apartment Transactions June 1-15, 2026

Most Active Areas

| Area | Transactions | Median Ticket | Median Price |

| Madinat Al Mataar | 1,507 | AED 674,000 | AED 1,718 psf |

| Jumeirah Village Circle | 319 | AED 1.07 Mn | AED 1,451 psf |

| Al Thanyah Fifth | 215 | AED 2.27 Mn | AED 2,662 psf |

| Dubai Land Residence Complex | 178 | AED 808,000 | AED 1,415 psf |

| Jabal Ali First | 176 | AED 1.85 Mn | AED 1,694 psf |

| Arjan | 148 | AED 862,000 | AED 1,711 psf |

| Business Bay | 142 | AED 1.87 Mn | AED 2,143 psf |

The five most active areas accounted for approximately 45.5% of all apartment transactions, highlighting the degree to which market activity remains concentrated within a relatively small number of locations.

Most Active Projects

| Project | Transactions |

| AZIZI VENICE 14 | 678 |

| ELTIERA VIEWS | 198 |

| AZIZI VENICE 9 | 146 |

| Azizi Venice 6 | 95 |

| DAMAC Lagoons Valencia | 93 |

| Skyhills Astra by HRE | 93 |

AZIZI VENICE 14 recorded 678 transactions during the period, accounting for approximately 12.9% of all apartment transactions captured within the dataset.

Brand Activity

Brand activity is estimated from project naming conventions and should not be interpreted as statutory developer market share.

| Brand | Transactions | Share |

| Azizi | 1,750 | 33.3% |

| Binghatti | 235 | 4.5% |

| DAMAC | 225 | 4.3% |

| Imtiaz | 159 | 3.0% |

| Samana | 127 | 2.4% |

Identified activity was concentrated around a relatively small number of project brands, with Azizi-branded developments accounting for approximately one-third of transactions where project naming patterns could be attributed to a specific brand.

Affordability Band Distribution June 1-15, 2026

Affordability Snapshot

The affordability profile of the market remained broadly consistent with May. The AED 1M–2M segment continued to represent the largest transaction band, while homes priced below AED 750,000 accounted for nearly one-third of activity. Despite an increase in median psf pricing, transaction activity remained concentrated within familiar affordability ranges, suggesting buyers were primarily purchasing smaller homes rather than materially increasing overall budgets.

Just 2.4% of transactions generated more than AED 1.2 billion in sales value, illustrating the disproportionate influence of the luxury segment.

Luxury Market Snapshot

| Metric | Value |

| AED 5M+ Transactions | 124 |

| Share of Transactions | 2.4% |

| AED 5M+ Sales Value | AED 1.206 Bn |

| Median Ticket | AED 6.66 Mn |

| Median Price | AED 3,572 psf |

| AED 10M+ Transactions | 31 |

Luxury transactions remained a relatively small component of market volume but continued to contribute disproportionately to overall sales value. While homes priced above AED 5 million represented just 2.4% of transactions, they generated approximately AED 1.2 billion in sales value, illustrating the disproportionate contribution of the luxury segment to overall market turnover.

Highest Apartment Sales

| Rank | Project | Area | Configuration | Sale Value |

| 1 | Solaya (5,7) | Jumeirah First | 3BR | AED 42.5 Mn |

| 2 | Como Residences | Palm Jumeirah | 4BR | AED 41.0 Mn |

| 3 | Baccarat Hotel & Residences | Burj Khalifa | 4BR | AED 40.0 Mn |

| 4 | The Meriva Collection | Palm Deira | 3BR | AED 33.1 Mn |

| 5 | The 118 | Burj Khalifa | 4BR | AED 30.7 Mn |

AIQYA Takeaway

The first half of June was characterised by concentration rather than broadening. Transaction activity remained heavily focused on compact off-plan inventory, while a relatively small number of locations, projects and launch platforms accounted for a significant share of market activity.

Dubai South continued to function as the market’s primary transaction hub, supported by large-scale launch activity and investor-oriented inventory. At the same time, the affordability profile of the market remained remarkably stable, with the AED 1M–2M segment continuing to represent the largest share of transactions.

The data suggests that Dubai’s apartment market remains driven by three forces: compact homes as the liquidity engine, developer launches as the transaction catalyst, and premium waterfront residences as the value anchors of the luxury segment.

Data Source & Methodology

Source: Dubai Land Department registered transaction dataset.

Scope: Residential, Freehold, Unit, Flats only.

Period: June 1–15, 2026.

Included procedures: Sale, Sell – Pre Registration, Sale on Payment Plan.

Excluded: mortgages, grants, delayed sales, lease-to-own, commercial assets, offices, shops, hotel apartments, villas and plots.

Price metric: AED per sq ft calculated using registered transaction value divided by unit area.

Brand activity: estimated from project naming patterns where no separate statutory developer field was available.

Figures are based on official registered datasets. Minor gaps may exist due to naming inconsistencies or exclusions. Report is intended for insight and education, not financial advice.

You may also like:

Dubai Residential Market May 2026 Data Snapshot