Dubai Housing Supply patterns during April and mid-May 2026 reveal how launch sequencing, rental demand, and compact apartment pipelines continue shaping the city’s next residential cycle.

This article continues AIQYA’s April–Mid May 2026 Dubai residential market study, focusing on rental trends, supply expansion, developer activity, and future market direction.

Luxury developments shape perception. Compact apartment launches continue shaping liquidity.

Buyer Profile & Demand Lens

One of the clearest themes running through Q2 is that Dubai’s residential market can no longer be understood through a single buyer archetype.

The city is now attracting multiple layers of demand simultaneously, each responding to different motivations, different risk tolerances, and different definitions of value.

This layered demand structure is one reason Dubai’s market is often misread through overly simplified narratives.

The same quarter can simultaneously produce:

- aggressive compact-unit absorption,

- stable family-home demand,

- and ultra-prime benchmark sales above AED 100M.

These are not isolated anomalies. They are different buyer ecosystems operating within the same city.

Dubai Residential Activity Corridors – May 1-15, 2026 Snapshot

The Investor Remains the Dominant Market Force

The largest share of transaction activity continues to come from investor-oriented demand.

This is especially visible across:

- studios,

- 1BR apartments,

- emerging launch corridors,

- and payment-plan-driven projects.

Typical investor priorities during Q2 included:

- lower entry tickets,

- yield potential,

- payment flexibility,

- resale liquidity,

- and faster project absorption.

| Investor Preference | Why It Matters |

| Compact layouts | Lower capital exposure |

| Flexible payment plans | Easier portfolio entry |

| High-activity corridors | Stronger liquidity |

| Off-plan launches | Early pricing access |

| Newer communities | Tenant appeal |

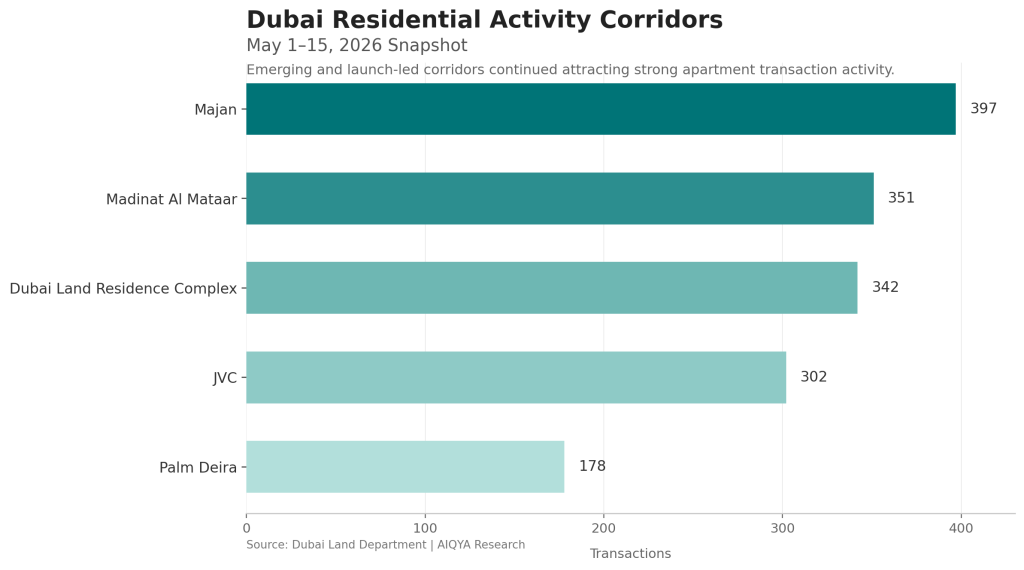

This explains why projects within:

- JVC,

- DLRC,

- Majan,

- and Madinat Al Mataar

continued attracting strong transactional momentum.

For many investors, these locations represent a balance between affordability and scalability.

End-Users Are Becoming More Visible

While investors still dominate transaction count, another layer of demand is gradually becoming more visible across the market: long-term residents.

This segment behaves differently.

End-users typically prioritize:

- livability,

- schools,

- community maturity,

- commute practicality,

- green space,

- and functional layouts.

They also tend to evaluate:

- construction quality,

- developer trust,

- handover confidence,

- and long-term maintenance more closely than short-cycle investors.

This demand is more visible in:

- larger 2BR and 3BR apartments,

- established communities,

- and projects positioned around lifestyle rather than pure yield.

📝 Interpretation

As Dubai matures as a long-term residential city, end-user demand is gradually becoming more structurally important even if it remains less visible in raw transaction counts.

The Upgrader Market Is Becoming More Selective

Another important Q2 pattern was the growing selectivity among upper-mid and upgrader buyers.

Unlike investors entering compact units, this segment tends to:

- compare projects more deeply,

- evaluate long-term livability,

- and exhibit lower tolerance for compromised layouts or inflated pricing.

Their decisions are influenced by:

- spatial quality,

- community environment,

- natural light,

- privacy,

- and overall residential experience.

This is where the market begins moving away from transactional logic and closer toward architectural and lifestyle logic.

This segment evaluates permanence more carefully than transactional momentum.

Global Capital Continues to Influence the Premium Market

At the top end of the market, Dubai continues attracting international wealth flows into:

- waterfront residences,

- branded developments,

- and ultra-prime inventory.

These buyers often behave differently from local investors.

Their motivations can include:

- geographic diversification,

- wealth preservation,

- lifestyle migration,

- and global asset allocation.

Q2 benchmark transactions once again reinforced the presence of this buyer class, particularly across premium branded inventory.

Yet despite their visibility, they remain a relatively concentrated portion of the broader market.

🧭 AIQYA Insight

The premium segment shapes international perception of Dubai. The compact and mid-market segments continue shaping actual market liquidity.

Both matter, but they influence the market in very different ways.

The Market Is Largely Reflecting Life Stages

Perhaps the most important shift visible in Q2 is that Dubai’s housing market is no longer responding only to investment behavior. Increasingly, it is responding to life-stage behavior.

| Buyer Type | Core Motivation |

| Early investors | Entry and yield |

| Portfolio investors | Liquidity and scalability |

| Young professionals | Urban access |

| Families | Stability and livability |

| Upgraders | Lifestyle quality |

| Global HNWIs | Capital preservation and prestige |

This creates a much more layered residential ecosystem than Dubai had a decade ago.

The city is gradually evolving from:

- a transactional property market,

toward: - a multi-layered urban housing system.

That transition may ultimately become one of the most important long-term stories shaping Dubai real estate.

Dubai Rental Yield Logic by Configuration

Rental Trends & Yield Outlook

While sales activity continued dominating headlines through Q2, the rental market quietly reinforced another important reality: Dubai’s residential engine still depends heavily on income-producing apartments.

Rental demand remained resilient across much of the city, particularly within compact and mid-market apartment clusters where affordability and accessibility continue driving tenant movement.

Rental performance is once again becoming central to investment decision-making.

The relationship between pricing and rental performance is becoming important because many investor decisions are now being shaped less by speculative appreciation and more by yield sustainability.

Rental Market Snapshot – May 1–15 Dataset

| Metric | Value |

| Cleaned Rental Contracts | 13,961 |

| Median Annual Rent | AED 68,250 |

| Median Rent PSF | AED 87.15 |

The rental market remains heavily concentrated in compact apartment formats, mirroring the structure seen on the sales side.

Studios and 1BR apartments continue forming the backbone of:

- tenant demand,

- investor participation,

- and yield-driven acquisition.

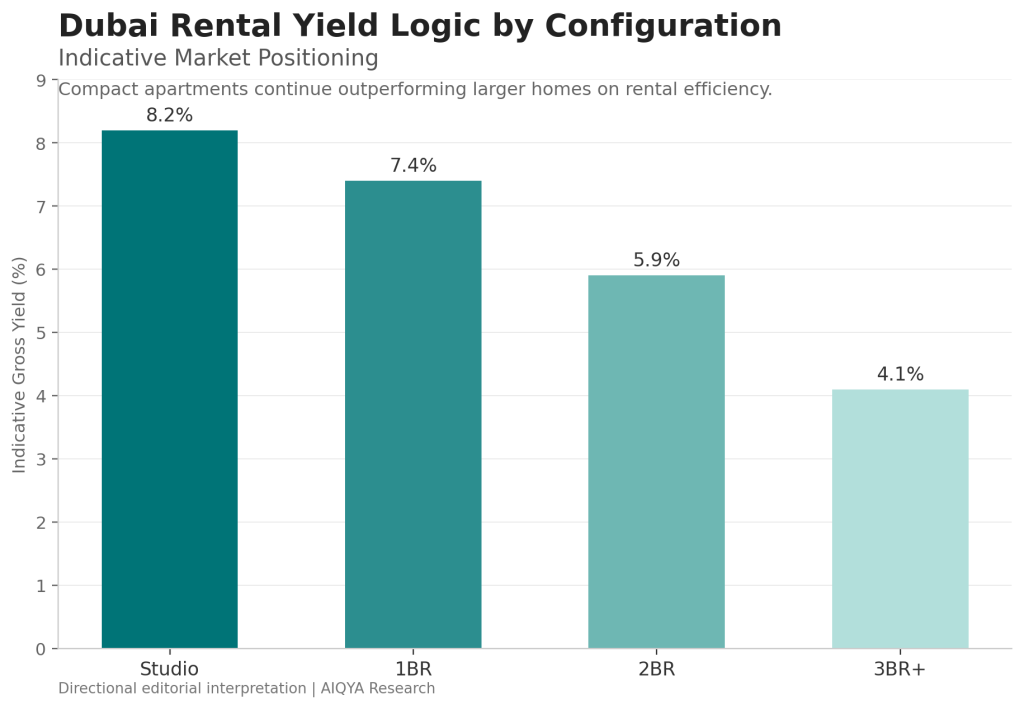

Compact Apartments Continue Delivering Stronger Yield Logic

One of the clearest patterns visible across the quarter is that smaller apartments continue offering stronger rental efficiency than larger homes.

| Configuration | Typical Yield Behavior |

| Studio | Highest gross yield potential |

| 1BR | Strong balance of liquidity and yield |

| 2BR | Moderate yield, stronger tenant stability |

| 3BR+ | Lower yield, higher lifestyle orientation |

This explains why investor activity remains heavily concentrated around compact inventory despite rising launch prices in several corridors.

📝 Interpretation

Compact apartments remain deeply tied to yield logic and tenant depth.

They are easier to lease, easier to circulate, and generally maintain broader tenant demand across economic cycles.

Rental Demand Remains Strong in Emerging Corridors

Several of the city’s highest-activity apartment corridors continue showing resilient rental participation, particularly in:

- JVC,

- Dubai Land Residence Complex,

- Majan,

- and surrounding mid-market clusters.

These locations increasingly attract:

- young professionals,

- newly relocated residents,

- and affordability-sensitive tenants seeking newer inventory.

The appeal often comes from a combination of:

- lower rent relative to core districts,

- newer building stock,

- integrated amenities,

- and improving infrastructure access.

This reinforces why these same corridors also continue attracting investor demand on the sales side.

The rental and ownership ecosystems continues feed each other.

Yield Compression Is Slowly Emerging in Select Segments

Although rental demand remains healthy, another subtle Q2 trend is beginning to appear: yield compression in parts of the market where sale prices have accelerated faster than rents.

This is particularly relevant in:

- premium launches,

- branded inventory,

- and certain high-visibility investor corridors.

As launch pricing rises, rental growth does not always keep pace proportionally.

That creates a narrowing spread between:

- acquisition cost,

- and annual rental income.

🧭 AIQYA Insight

The market is gradually separating into:

- yield-driven inventory,

- and capital-preservation inventory.

Not every project is being purchased for the same financial logic anymore.

Some are bought primarily for income efficiency. Others are treated as long-term wealth assets.

Rental Anomalies Need Careful Interpretation

The cleaned rental dataset also revealed several extreme-value rental registrations, including one contract with unusually elevated values far outside normal residential ranges.

These are likely:

- bulk registrations,

- institutional agreements,

- or reporting anomalies.

This is an important reminder that raw benchmark figures should be interpreted cautiously.

AIQYA’s approach benefits from filtering market spectacle from market structure.

A single extraordinary rental contract may generate attention, but it does not define everyday residential demand across the city.

The Relationship Between Rentals and Sales Is Tightening

Perhaps the most important long-term signal from Q2 is how closely the rental and sales ecosystems are now intertwined.

Investors increasingly evaluate:

- projected rent,

- occupancy confidence,

- tenant depth,

- and exit liquidity

before entering projects.

Developers, in turn, has evolved into designing projects around:

- rentable formats,

- efficient unit planning,

- and tenant-friendly amenity structures.

This creates a residential market where rental behavior begins to influences:

- launch success,

- pricing power,

- and long-term absorption.

Dubai’s housing market is no longer moving only through capital appreciation narratives. Rental performance is once again becoming central to investment decision-making.

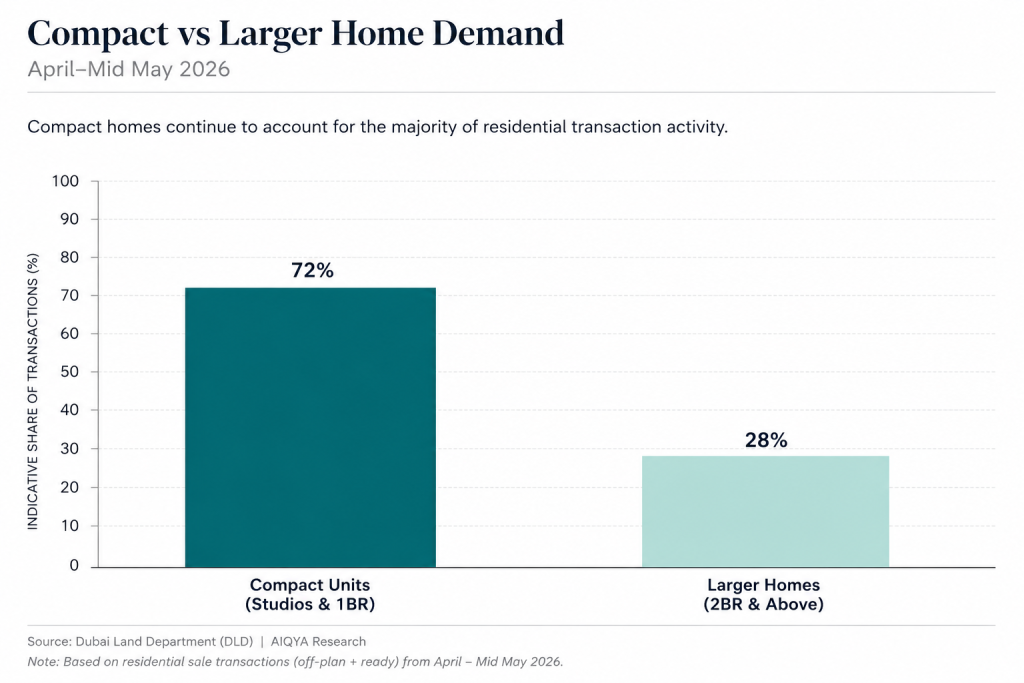

Compact vs Larger Home Demand

Configuration Spotlight – Project-Level Breakdown

The project-level mix adds another layer to the Q2 story. Dubai’s market is not only compact-led at the city level. Many of the strongest launches are deliberately built around compact absorption.

What the Project Mix Shows

| Project Type | Dominant Configuration | Typical Buyer Logic |

| Investor-led launches | Studio & 1BR | Yield and liquidity |

| Mid-market projects | 1BR & 2BR | Balanced investor/end-user demand |

| Family-oriented communities | 2BR & 3BR | Long-term livability |

| Premium branded inventory | Larger layouts | Prestige and capital preservation |

The strongest transaction clusters in May were led by projects where the unit mix aligned closely with market liquidity.

This is why 1BR-heavy launches often outperform on volume. They sit in the sweet spot between:

- livability,

- rental depth,

- resale liquidity,

- and manageable ticket size.

Studios support rapid investor entry, but the 1BR remains the more balanced product in Dubai’s current apartment cycle.

What Configuration Mix Reveals

A project’s configuration mix now tells us almost as much as its location.

A compact-heavy launch usually signals:

- investor-first positioning,

- faster absorption expectations,

- lower entry ticket strategy,

- and stronger rental-yield marketing.

A 2BR or 3BR-heavy project points toward a different market:

- families,

- upgraders,

- longer holding periods,

- and lifestyle-led demand.

AIQYA Insight

The most useful question is no longer simply:

“Where is the project located?”

It is also:

“What kind of buyer is the configuration mix designed to attract?”

That one question often reveals the project’s true market intent.

Risks & Watchpoints

Dubai’s residential market remains active, but Q2 also shows why the next phase needs sharper reading.

The bigger challenge is not vanishing demand, but interpreting demand correctly. The risk is that different parts of the market are now being mistaken for one another.

Key Watchpoints

| Watchpoint | Why It Matters |

| Launch concentration | Heavy off-plan dependence can inflate activity in specific months |

| Price composition | Premium launches can lift median pricing without broad repricing |

| Yield compression | Sale prices may rise faster than rents in some corridors |

| Compact-unit oversupply | Investor-heavy stock needs sustained tenant demand |

| Rental data anomalies | Extreme contracts should be validated before interpretation |

| Handover pipeline | Future supply may test weaker corridors |

| Payment-plan dependency | Buyer behavior may shift if financing conditions tighten |

The most important watchpoint is supply sequencing.

If large volumes of compact apartments are handed over within a short window, the market will need equally strong rental absorption to maintain yield confidence.

That does not mean oversupply is inevitable. It means corridor-level monitoring becomes more important than citywide conclusions.

AIQYA Insight

Dubai’s housing market is not structurally weak, but it is becoming more layered and selective. It is becoming complex.

The strongest assets will likely be those with:

- real tenant depth,

- credible developers,

- efficient layouts,

- mature community infrastructure,

- and pricing that still leaves room for rental logic.

The weaker assets may not fail immediately, but they could become harder to exit when buyers become more selective.

Supply Snapshot – What’s in the Pipeline

One of the defining characteristics of Dubai’s residential market today is that supply is no longer arriving in isolated waves. It is arriving as a continuous urban expansion system.

Q2 reinforced how deeply the market now depends on active launch pipelines across multiple growth corridors simultaneously.

Where New Supply Is Concentrating

Several corridors continued attracting the highest concentration of launch activity and transaction absorption during the quarter.

| Corridor | Current Supply Character |

| Majan | Emerging mid-market apartment cluster |

| DLRC | High-volume investor inventory |

| JVC | Mature launch ecosystem |

| Madinat Al Mataar | Expansion-led growth corridor |

| DAMAC Lagoons region | Lifestyle suburban expansion |

These areas share common structural advantages:

- scalable land availability,

- strong compatibility with installment-led purchasing,

- and pricing bands that remain accessible to broader investor pools.

This is where much of Dubai’s future apartment inventory is currently accumulating.

Growth Corridors Continue Expanding

One of the quieter but more important Q2 trends is the continued outward movement of transactional activity.

Many of the strongest-performing corridors are no longer located within traditional premium districts. Instead, they sit along expanding suburban and peripheral growth belts where:

- land remains more scalable,

- masterplans are larger,

- and pricing remains comparatively accessible.

📝 Interpretation

Dubai’s residential expansion increasingly resembles a corridor-based urban model rather than a single concentrated city core.

That changes how future value may emerge across the market.

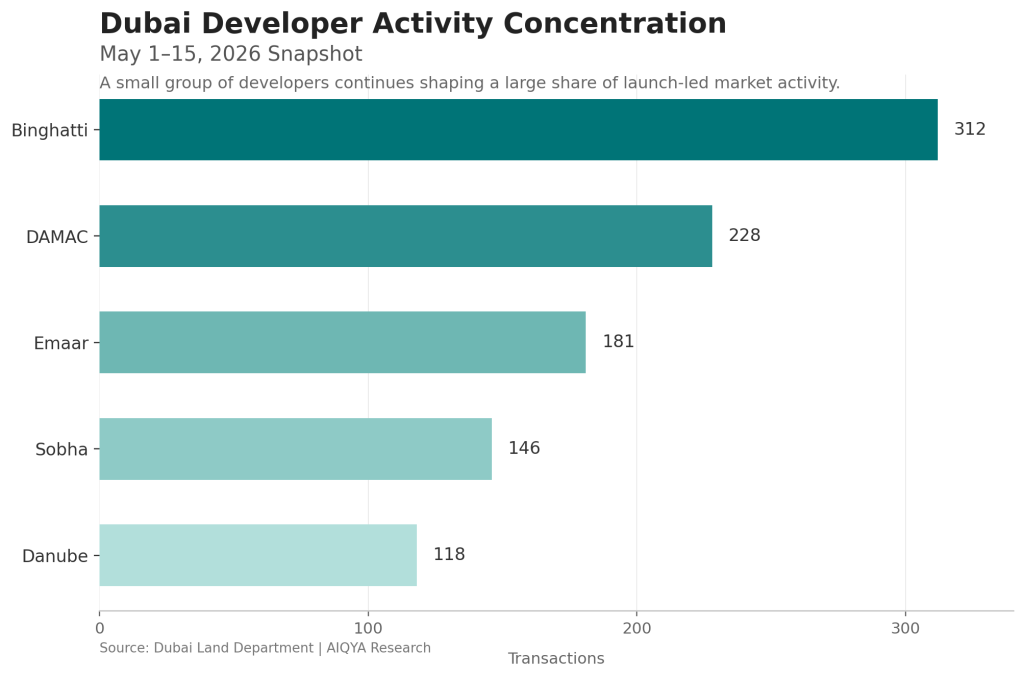

Dubai Developer Activity Concentration

Supply Is Becoming More Calibrated

Another notable shift is that developers appear to be disciplined in how inventory is phased.

Rather than releasing massive inventory blocks simultaneously, many projects now follow:

- staggered launches,

- phased tower releases,

- and payment-plan sequencing designed to maintain absorption momentum.

This reflects a more mature supply strategy than earlier cycles where rapid inventory dumping often destabilized pricing.

Several developers now appear highly conscious of:

- psychological affordability,

- investor pacing,

- and maintaining scarcity perception during active sales periods.

Compact Inventory Continues Dominating the Pipeline

The future pipeline remains heavily weighted toward:

- studios,

- 1BR apartments,

- and efficient 2BR layouts.

This aligns directly with the market’s current liquidity profile.

Developers are increasingly building where transaction velocity already exists.

| Pipeline Trend | Market Meaning |

| Smaller units | Faster absorption |

| Efficient layouts | Better affordability alignment |

| Mixed-use communities | Stronger tenant ecosystems |

| Branded launches | Premium pricing leverage |

| Lifestyle-led suburbs | Long-term expansion strategy |

🧭 AIQYA Insight

Future supply appears more optimized around absorption efficiency rather than sheer scale. It is being designed around maximum absorption efficiency.

That distinction may define the next phase of the city’s apartment market.

The Real Question Is Not Supply Alone

Dubai has historically been viewed through the lens of supply risk. Q2 suggests a more nuanced framework is needed.

The more important question may now be:

Where is supply arriving, and who is it designed for?

Some corridors continue showing:

- deep investor participation,

- strong tenant depth,

- and active transaction velocity.

Others may eventually face greater pressure if:

- handovers cluster too heavily,

- rental demand softens,

- or investor exits increase simultaneously.

This means future market stability may increasingly depend on corridor-level balance rather than citywide supply numbers alone.

A City Building Multiple Housing Futures Simultaneously

The pipeline also reveals something broader about Dubai’s urban evolution.

The city is simultaneously building:

- investor housing,

- family housing,

- suburban lifestyle communities,

- branded luxury districts,

- and globally marketed trophy inventory.

These are not all competing for the same buyer.

That is why Dubai’s residential market behaves less like a single housing system and more like several overlapping residential economies moving together at different speeds.

Plot Transactions & Land Signals

For this May 1–15 residential apartment reading, plots should be treated as a separate signal rather than merged into the main housing numbers.

The apartment market tells us about buyer liquidity.

The land market tells us about developer conviction.

That distinction is important.

Why Land Signals Matter

| Land Activity Pattern | Possible Market Interpretation |

| Outer corridor acquisitions | Future apartment expansion |

| Mid-market land accumulation | Continued compact housing focus |

| Large masterplan deals | Long-duration suburban growth |

| Premium waterfront plots | Luxury supply continuation |

| Land Signal | What It Suggests |

| Rising plot activity | Developer confidence in future launches |

| Higher land values | Expectations of stronger end-pricing |

| Concentration in growth corridors | Future supply clusters |

| Large residential land deals | Longer-term development pipeline |

Plot transactions are not directly comparable to apartment sales, but they help explain where future supply may emerge.

Final Observations & Buyer Takeaways

Q2 2026 did not reveal a market losing momentum. It revealed a market becoming more internally differentiated.

Dubai is no longer behaving like a single-direction property cycle where every segment rises or slows together. The city now operates through layered residential ecosystems responding to different forms of demand.

Compact apartments continue functioning as the market’s liquidity engine. They dominate transaction activity because they align closely with:

- payment-plan accessibility,

- investor affordability,

- rental demand,

- and resale flexibility.

The AED 1M–2M segment remains the centre of gravity within this structure. It is where transaction velocity, tenant depth, and manageable ticket sizes still intersect most effectively.

At the same time, larger homes and family-oriented residences continue playing a quieter but stabilizing role. Their transaction volumes are lower, but their buyer intent is deeper. These homes are less dependent on rapid investor circulation and more connected to long-term residential confidence.

That layered structure is now central to how Dubai’s housing market operates.

One side of the market behaves like a high-liquidity investment system driven by launches, installment structures, and compact inventory. The other behaves more like an evolving global residential city shaped by lifestyle migration, settlement patterns, and long-duration living.

The luxury segment operates adjacent to both layers, often influencing perception more than actual market structure.

This quarter also reinforced how strongly developer sequencing now shapes transaction behavior. Off-plan dominance is no longer a temporary phase. It has become one of the foundational operating mechanics of Dubai’s residential ecosystem.

That brings both strengths and vulnerabilities.

The strengths are visible:

- strong liquidity,

- scalable housing production,

- active global capital participation,

- and broad investor accessibility.

The vulnerabilities are subtler:

- corridor-level supply concentration,

- yield compression in select launches,

- and increasing dependence on continual absorption momentum.

The most resilient projects over the coming cycles are likely to be those that combine:

- efficient layouts,

- credible developers,

- sustainable rental logic,

- strong tenant ecosystems,

- and genuine livability rather than purely speculative positioning.

For buyers, the market largely requires selectivity rather than broad optimism or broad pessimism.

For investors:

- rental mathematics matter more than headline excitement,

- liquidity matters more than spectacle,

- and exit depth matters more than launch marketing.

For end-users:

- community maturity,

- spatial quality,

- environmental comfort,

- and long-term liveability

are becoming very important as Dubai transitions toward a more permanent residential city.

🧭 AIQYA Insight

The most important takeaway from Q2 may be this:

Dubai’s residential market is no longer defined only by growth. It is now being shaped by how different forms of housing demand interact with one another.

And understanding that evolution now requires looking beyond headline prices and transaction volumes toward the deeper mechanics shaping how the city is actually being bought, lived in, rented, and built.

Data Source Attribution & Method Note

Dataset Scope

This report is based on cleaned and standardized residential transaction and rental datasets derived from official Dubai Land Department registrations covering:

- April 2026

- May 1–15 2026 directional activity

- Q2 2026 comparative interpretation

Scope applied throughout the report:

- Residential

- Freehold

- Units / Flats only

Excluded:

- Offices

- Shops

- Commercial assets

- Hotel rooms

- Mortgage registrations

- Delayed sales

- Lease-to-own structures

- Non-residential transfers

Sales Procedures Included

The following transaction procedures were included:

- Sale

- Sell – Pre Registration

- Sale on Payment Plan

Deduplication Method

Datasets were standardized and deduplicated using:

- Project Name

- Registration Date

- Unit Area

- Transaction Value

This approach minimizes duplicate registration noise while preserving transaction integrity.

Pricing Methodology

Median Price PSF

Calculated using:

Median values were used instead of averages wherever possible to reduce distortion from ultra-prime outliers.

Rental Yield Interpretation

Gross rental yield observations were directionally derived from:

- median annual rental values,

- median transaction ticket sizes,

- and configuration-level comparisons.

No projected or imputed yields were used.

Extreme-value rental anomalies and bulk registrations were excluded from narrative interpretation where appropriate.

Off-Plan vs Ready Classification

Primary and secondary market splits were directly derived from official DLD off-plan indicators without manual overrides.

Important Reading Note

Dubai’s residential market has started to behave as a composition-sensitive ecosystem where:

- launch timing,

- inventory mix,

- branded supply,

- and payment-plan sequencing

can materially influence monthly pricing and transaction metrics.

As a result, headline figures should be interpreted alongside:

- corridor activity,

- unit configuration mix,

- and market composition trends.

Disclaimer

Figures are based on official registered datasets and cleaned internal analysis methodologies. Minor gaps may exist due to naming inconsistencies, delayed registrations, bulk entries, or data exclusions.

This report is intended for research, education, and market interpretation purposes only and should not be treated as financial or investment advice.

Also Read

Inside Dubai’s Residential Liquidity Engine

The first part of this AIQYA market study examines transaction activity, off-plan dominance, pricing behavior, compact housing demand, and the evolving structure of Dubai’s residential market during April and mid-May 2026.

Dubai Residential Market Trends April–Mid May 2026

You may also like:

Dubai Residential Property Market April 2026 – What the Data Shows

Dubai Property Market Q1 2026: Structure, Pricing and Demand Trends