Dubai Residential Market Trends during April and mid-May 2026 reveal a housing market shaped less by broad acceleration and more by internal differentiation between liquidity-driven apartments, launch-led activity, and long-term residential demand.

- Market Overview

- Key Market Metrics – Q2 2026

- Price Trends & Market Interpretation – Q2 2026

- Primary vs Secondary Market Composition – Q2 2026

- Configuration Distribution – What Buyers Are Choosing

- Unit Size Trends & Market Signals

- Top Projects & Developer Activity

- Affordability Snapshot – Where Buyers Are Spending

This article is part of an ongoing AIQYA study examining Dubai’s residential market during April and mid-May 2026, covering liquidity trends, supply dynamics, rental movement, and evolving buyer behavior.

Compact homes continue functioning as the market’s liquidity engine.

Market Overview

Dubai’s residential market entered Q2 2026 with a noticeable shift in tone. Neither a collapse in demand nor an uncontrolled surge, but a market beginning to show internal differentiation.

The first quarter of the year was largely defined by launch-driven momentum. Off-plan projects continued to dominate transaction activity, compact homes remained the city’s liquidity engine, and developers successfully absorbed demand through staged payment structures rather than conventional mortgage-led buying.

By April and early May, however, another layer started becoming visible beneath the headline numbers.

Transaction activity remained elevated, but pricing behavior became more selective. Certain launch corridors continued to command strong absorption and premium pricing, while other segments appeared to stabilize after the sharper acceleration seen earlier in the year.

This distinction matters.

Much of the public conversation around Dubai’s property market tends to reduce the city into a single narrative: either overheating or cooling. The transaction data suggests something more nuanced. The market continuous to behaves like multiple parallel ecosystems operating at different speeds.

Compact investor-oriented apartments continue to circulate rapidly through launch cycles and payment-plan demand. Family-oriented homes and larger layouts, meanwhile, behave more like long-duration residential assets with comparatively lower churn but greater pricing stability.

The result is a housing market that appears active on the surface, but internally segmented by:

- ticket size,

- buyer intent,

- financing structure,

- launch timing,

- and corridor maturity.

Q2 also reinforced how heavily the city’s residential activity is now linked to supply sequencing. In several emerging corridors, transaction spikes corresponded less to organic resale activity and more to concentrated waves of developer inventory entering the market.

This has gradually transformed Dubai into a launch-responsive market where:

- timing matters almost as much as location,

- payment structure matters almost as much as pricing,

- and inventory release strategy shapes transaction momentum quarter by quarter.

At the same time, rental demand remained resilient across several mid-market apartment clusters. Gross yields in many compact-unit corridors continue to outperform larger residences, reinforcing investor preference toward smaller layouts despite rising launch prices in certain zones.

Another notable development during this period was the continued expansion of activity into outer growth corridors. Areas such as:

- Majan,

- Dubai Land Residence Complex,

- Madinat Al Mataar,

- and parts of JVC

continued attracting significant transaction volume, indicating that affordability-sensitive demand remains one of the strongest forces shaping the market.

The premium market also remained active, though in a more concentrated manner. High-ticket transactions and ultra-prime benchmark sales continued to appear across select luxury projects, but these transactions now behaved as isolated capital events rather than broad market indicators.

That distinction becomes important later in the report when interpreting pricing signals.

Because while trophy transactions attract headlines, the actual direction of Dubai’s residential market is still largely being determined by:

- compact apartments,

- mid-market launches,

- and the velocity of off-plan absorption.

In many ways, Q2 2026 revealed a city balancing two housing identities simultaneously:

- a global capital destination driven by branded luxury and investment flows,

- and a high-volume urban housing system powered by attainable apartments and structured developer financing.

That duality now sits at the center of Dubai’s residential market.

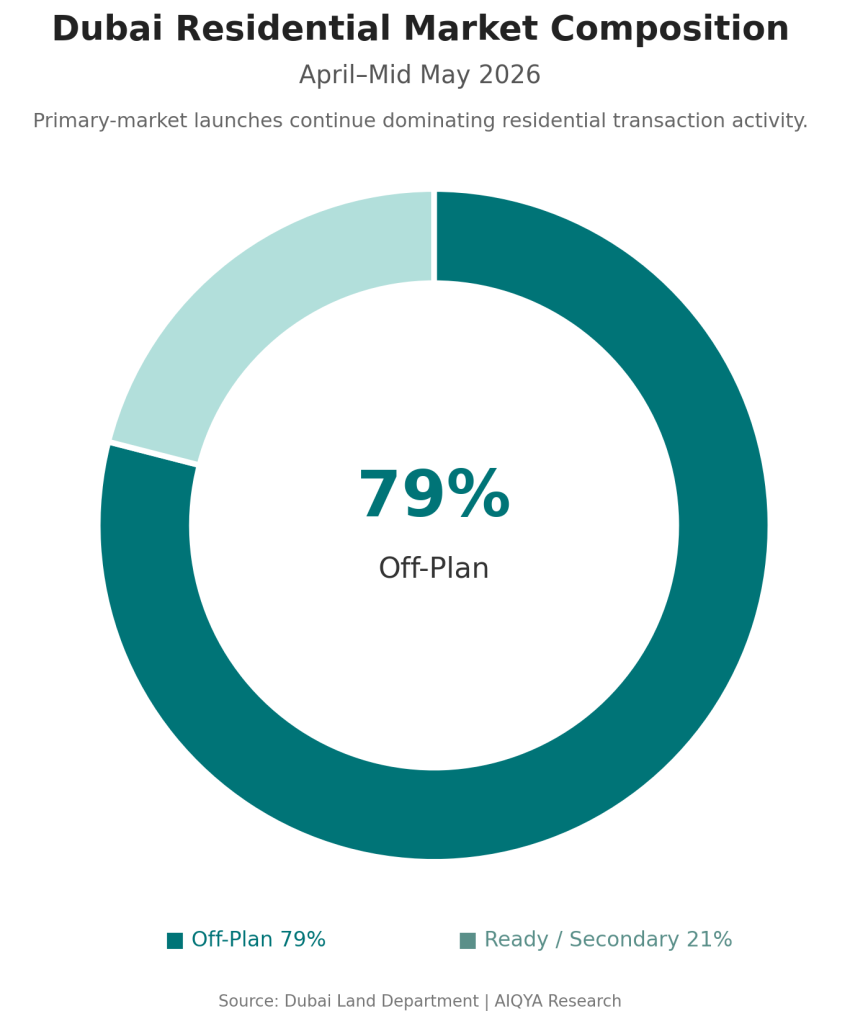

Dubai Residential Market Composition – April – Mid May 2026

Key Market Metrics – Q2 2026

The numbers from Q2 continue to reinforce a market that remains highly liquid, though is becoming segmented by product type and buyer profile.

The quarter did not show signs of a broad-based contraction. Instead, it reflected a market recalibrating after a particularly aggressive launch cycle earlier in the year.

The AED 1M–2M segment remains the centre of gravity within Dubai’s housing market.

Residential Freehold Transactions Snapshot

| Metric | Q2 2026 |

| Total Residential Transactions | 24,000+* |

| Off-Plan Share | ~78–82% |

| Ready Property Share | ~18–22% |

| Median Price | AED 1,700–1,850 psf |

| Median Ticket Size | AED 1.2M–1.5M |

| Dominant Configuration | 1BR |

| Strongest Activity Band | AED 1M–2M |

| Primary Market Driver | Developer Launches |

*Based on April and May directional run-rates from cleaned DLD datasets.

The Market Is Still Being Driven by Off-Plan Liquidity

One of the clearest signals across the quarter was the continued dominance of off-plan transactions.

In several periods during Q2, off-plan inventory accounted for nearly four out of every five residential transactions.

| Market Composition | Approx. Share |

| Off-Plan | 79% |

| Ready / Secondary | 21% |

📝 Interpretation

This is no longer a temporary cycle. Developer-led absorption has become the structural backbone of Dubai’s residential market.

The city’s transaction engine now depends on:

- phased inventory releases,

- flexible payment structures,

- and launch-led buyer momentum.

Traditional resale-led activity continues to exist, but it no longer defines the broader direction of the market.

Pricing Remained Elevated, But More Selective

Median pricing across the quarter largely remained within the AED 1,700–1,850 psf range depending on launch composition and inventory mix.

| Period | Median Price PSF |

| Q1 2026 Baseline | AED 1,754 |

| April 2026 | AED 1,865 |

| May 1–15 2026 | AED 1,689 |

At first glance, the decline from April to May could appear like softening demand. The underlying composition tells a more nuanced story.

April’s pricing was heavily influenced by:

- premium launches,

- branded inventory,

- and concentrated off-plan absorption.

By May, transaction activity shifted slightly back toward broader mid-market inventory.

🧭 AIQYA Insight

Dubai’s pricing behavior now reflects inventory composition rather than uniform market-wide appreciation.

That distinction is critical.

A launch-heavy month can rapidly elevate median pricing without necessarily indicating broad repricing across the city.

Ticket Sizes Continue to Reveal Buyer Psychology

The median transaction ticket continued hovering around the AED 1.2M–1.5M range through the quarter.

This remains one of the most important indicators in the market.

Why?

Because it highlights where real liquidity sits.

| Ticket Band | Market Behavior |

| Under AED 1M | Entry investor activity |

| AED 1M–2M | Core market liquidity |

| AED 2M–5M | Upgrader & upper-mid demand |

| AED 5M+ | Luxury & global capital flows |

The AED 1M–2M segment continues functioning as Dubai’s transactional core.

It represents the zone where:

- affordability,

- payment-plan flexibility,

- rental viability,

- and investor accessibility

intersect most efficiently.

This is also why compact apartments continue dominating transaction volumes across emerging corridors.

Benchmark Transactions Continue to Distort Headlines

The quarter also recorded several ultra-high-value transactions, including benchmark sales above AED 100M.

One of the highest recorded apartment transactions during the May 1–15 dataset exceeded:

- AED 112M,

- with pricing above AED 7,300 psf.

These transactions are important market signals, but they should not be mistaken for broad pricing benchmarks.

📝 Interpretation

Ultra-prime sales is beginning to behave as isolated capital events tied to:

- branded inventory,

- waterfront scarcity,

- or global wealth allocation.

The broader housing market still moves according to:

- compact apartment liquidity,

- launch sequencing,

- and payment-plan absorption.

That distinction separates market spectacle from market structure.

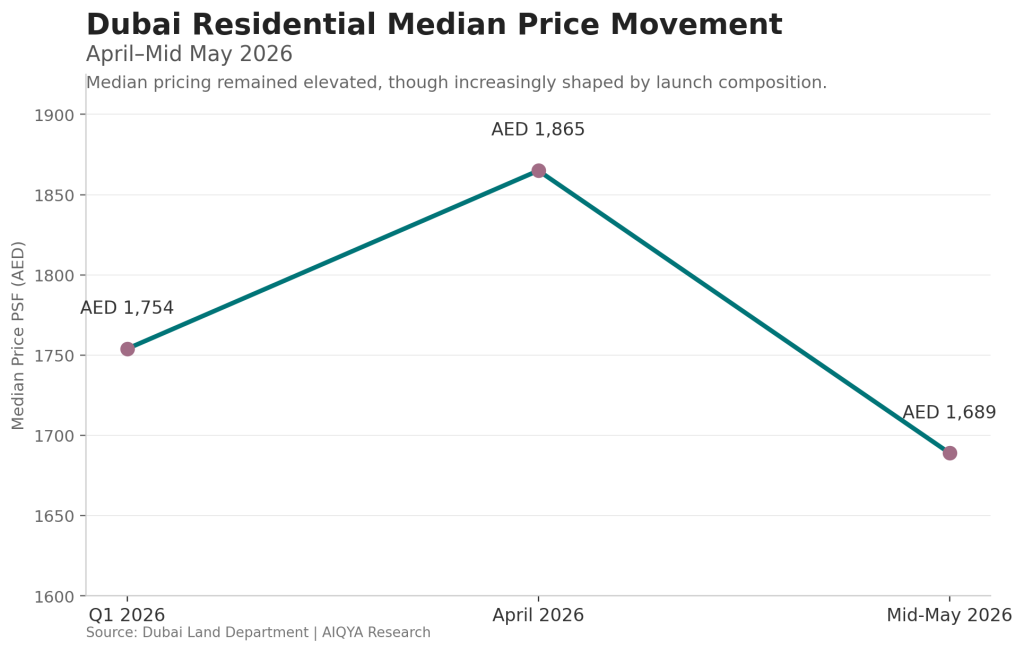

Dubai Residential Median Price Movement – April-Mid May 2026

Price Trends & Market Interpretation – Q2 2026

The pricing story in Dubai during Q2 was less about acceleration and more about composition.

Headline numbers continued to suggest strength. Median pricing remained elevated by historical standards, premium launches continued entering the market, and select benchmark transactions pushed into ultra-prime territory. Yet beneath those figures, the market now revealed signs of differentiation between liquidity-driven housing and capital-driven housing.

Median Pricing Continued to Hold at Elevated Levels

Across the quarter, median residential pricing largely fluctuated within a relatively narrow band.

| Period | Median Price PSF |

| Q1 2026 | AED 1,754 |

| April 2026 | AED 1,865 |

| May 1–15 2026 | AED 1,689 |

The movement between April and May is particularly important because it demonstrates how sensitive Dubai’s pricing metrics have become to launch composition.

April’s sharper pricing was influenced by:

- branded inventory,

- premium launches,

- higher-ticket project releases,

- and stronger concentration of off-plan activity.

May, by comparison, saw greater participation from broader mid-market inventory and compact apartments.

📝 Interpretation

Different parts of the market are now responding to entirely different forces.

Certain launches are achieving substantial pricing power, while large portions of the broader market continue operating within affordability-sensitive ranges.

This creates the appearance of a rapidly rising market in headline figures even when much of the underlying housing stock remains relatively stable.

Dubai Is Increasingly Behaving Like a Multi-Speed Housing Market

One of the clearest structural shifts visible in Q2 is the widening separation between three distinct layers of the market.

| Market Layer | Primary Driver | Typical Buyer |

| Compact Mid-Market Apartments | Yield & affordability | Investors |

| Family-Oriented Residences | Long-term living | End-users & upgraders |

| Ultra-Prime / Branded Inventory | Global capital allocation | HNWIs & international buyers |

These segments are no longer moving in perfect alignment.

Compact apartments continue experiencing:

- high transaction velocity,

- aggressive launch absorption,

- and strong investor participation.

Family-oriented homes show comparatively slower churn but greater stability.

Meanwhile, ultra-prime inventory behaves almost independently from the broader residential market.

🧭 AIQYA Insight

Dubai is gradually evolving from a singular property market into a layered residential ecosystem where each segment responds to different economic forces.

Headline pricing now reveals less about the city as a whole and more about which segments are currently leading activity.

Compact Homes Continue Defining the Market Direction

The strongest transactional activity during Q2 remained concentrated in:

- studios,

- 1BR apartments,

- and lower-to-mid ticket inventory.

| Configuration | Approx. Share of Transactions |

| Studio | ~30% |

| 1BR | ~42% |

| 2BR | ~21% |

| 3BR+ | ~7% |

Studios and 1BR apartments together represented roughly three-quarters of all residential activity in several periods during the quarter.

This concentration matters because these units:

- respond fastest to payment-plan structures,

- attract the broadest investor pool,

- and maintain stronger liquidity during shifting market conditions.

They are effectively the circulation system of Dubai’s housing market.

Larger residences behave differently. They transact less frequently, involve longer decision cycles, and are more closely tied to lifestyle stability than short-term capital movement.

Price Growth Is Becoming more Corridor-Specific

Another important Q2 trend was the uneven distribution of pricing strength across the city.

Several emerging corridors continued showing elevated transaction activity despite softer narratives circulating in parts of the global media.

Among the strongest recurring activity zones:

- Majan,

- Dubai Land Residence Complex,

- Madinat Al Mataar,

- and JVC

continued demonstrating sustained absorption.

These areas largely benefit from a combination of:

- lower entry pricing,

- newer inventory,

- investor familiarity,

- and infrastructure adjacency.

At the same time, premium coastal and branded districts continued pushing benchmark pricing higher through isolated luxury transactions.

The result is a city where:

- transaction activity may remain strong,

- while pricing experiences localized acceleration rather than uniform appreciation.

Benchmark Transactions Are Changing Market Perception

Q2 also highlighted how a relatively small number of ultra-prime transactions can influence broader market sentiment.

A handful of high-value branded and waterfront sales generated substantial visibility due to:

- record ticket sizes,

- elevated psf benchmarks,

- and international buyer participation.

Yet these transactions represent only a very small portion of total market activity.

📝 Interpretation

Dubai’s residential market still derives most of its liquidity from attainable apartments rather than trophy residences.

The city’s long-term housing momentum is currently being sustained less by ultra-luxury spectacle and more by the continual absorption of compact inventory across expanding residential corridors.

That difference between perception and structural reality is becoming important in understanding the market correctly.

Primary vs Secondary Market Composition – Q2 2026

If one metric defines Dubai’s residential market today, it is the overwhelming dominance of the primary market.

The city has gradually shifted from being a resale-driven ecosystem into one where developer launches shape both transaction momentum and buyer psychology. Q2 2026 reinforced this transformation with unusual clarity.

Across multiple datasets during the quarter, off-plan transactions consistently accounted for nearly four-fifths of all residential activity.

| Market Segment | Approx. Share |

| Off-Plan / Primary | 79–82% |

| Ready / Secondary | 18–21% |

This is no longer a temporary spike in off-plan activity. It reflects a structural evolution in how housing is bought, sold, and financed in Dubai.

The Market Now Moves to the Rhythm of Launches

Historically, many mature property markets derive stability from secondary-market circulation. Dubai continuous to operate differently.

In the current environment:

- launches generate attention,

- payment plans generate accessibility,

- and phased inventory releases generate transaction velocity.

The market’s momentum now closely follows the cadence of developer activity.

Several of the quarter’s highest-volume projects were newly launched or recently released phases, including inventory across:

- Majan,

- Dubai Land Residence Complex,

- Madinat Al Mataar,

- and outer growth corridors.

| High-Activity Projects | Indicative Signal |

| Binghatti Skyflame | Aggressive launch absorption |

| DAMAC Lagoons | Lifestyle-led suburban demand |

| The Wilds Residences | Premium low-density positioning |

| Multiple JVC launches | Compact investor liquidity |

📝 Interpretation

Dubai’s housing market behaves like a supply-responsive ecosystem rather than a purely demand-responsive one.

The sequencing of launches now shapes monthly transaction behavior almost as strongly as macroeconomic conditions.

Why Buyers Continue Choosing Off-Plan

The dominance of off-plan inventory is not being driven by speculation alone. Several structural factors continue supporting primary-market preference.

1. Lower Initial Capital Requirement

Developer payment structures allow buyers to enter the market with significantly lower upfront liquidity compared to conventional mortgage-heavy systems.

For many investors, this reduces:

- immediate cash exposure,

- financing pressure,

- and short-term holding costs.

2. Access to Newer Inventory

Many buyers continue preferring:

- modern layouts,

- newer community infrastructure,

- updated amenities,

- and integrated mixed-use developments.

This naturally shifts demand toward primary launches rather than older secondary stock.

3. Installment-Based Market Psychology

Dubai’s property market largely functions around installment culture rather than traditional ownership culture.

This is particularly visible in:

- compact apartments,

- investor-oriented projects,

- and outer growth corridors.

🧭 AIQYA Insight

Payment plans are no longer just sales tools. They now shape how large parts of Dubai’s housing market function.

The structure of financing now influences demand almost as much as location itself.

The Secondary Market Still Plays a Different Role

Although smaller in transaction share, the ready market continues performing an important stabilizing function.

Secondary inventory remains relevant for:

- end-users seeking immediate occupancy,

- buyers prioritizing established communities,

- rental-income investors,

- and families seeking certainty over launch risk.

The resale market also behaves differently during volatility.

While off-plan activity can accelerate rapidly during strong launch cycles, secondary-market pricing often moves more gradually because it is tied more closely to:

- lived communities,

- operational buildings,

- and realized rental performance.

This creates an interesting dual structure within Dubai’s housing ecosystem:

- the primary market drives velocity,

- while the secondary market anchors continuity.

The Rise of Launch Corridors

Another defining Q2 pattern was the emergence of what can now be described as “launch corridors.”

These are districts where transaction activity is concentrated around continuous waves of developer inventory entering the market.

Among the clearest examples:

- Majan,

- Dubai Land Residence Complex,

- Madinat Al Mataar,

- and portions of JVC.

These locations share several characteristics:

- comparatively lower entry pricing,

- large land availability,

- scalable apartment inventory,

- and strong compatibility with installment-led purchasing.

The result is a residential geography shaped by developer sequencing rather than traditional urban hierarchy alone.

A Market Becoming More Cyclical Internally

The growing dominance of the primary market also introduces a new layer of cyclicality into Dubai’s housing system.

When launches accelerate:

- transaction volumes surge,

- off-plan share rises,

- and pricing metrics can move rapidly.

When launch pipelines temporarily slow:

- market activity can soften quickly,

- even if underlying end-user demand remains stable.

📝 Interpretation

This means quarterly market readings now need contextual interpretation.

A slowdown in transaction velocity may not necessarily indicate weakening demand. It may simply reflect:

- fewer launches,

- delayed inventory releases,

- or changes in developer sequencing.

That is one of the most important structural realities shaping Dubai’s residential market today.

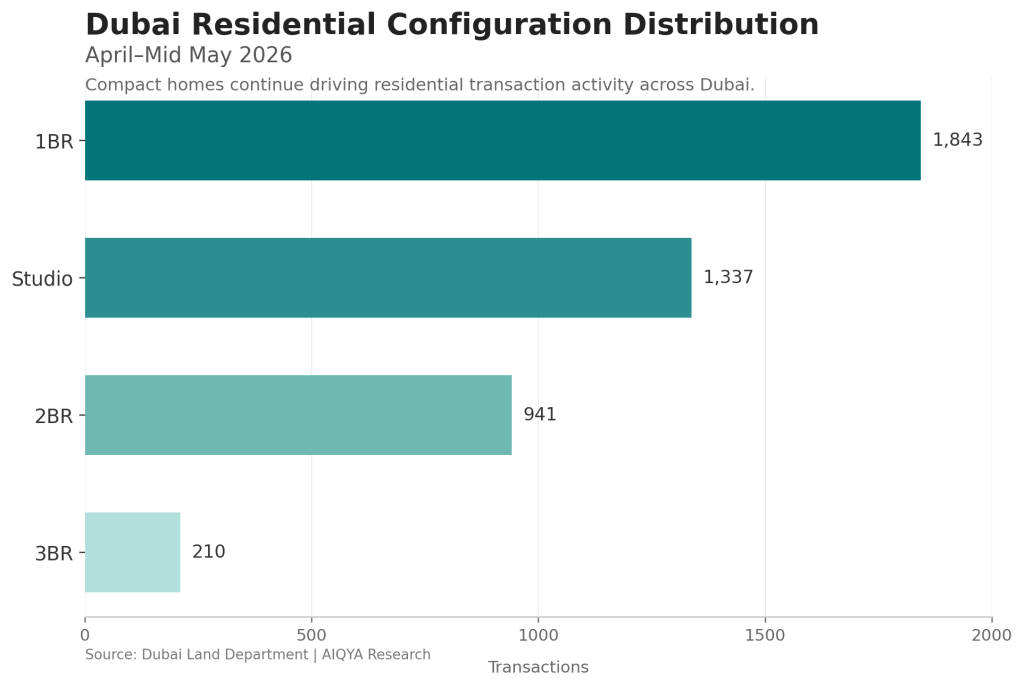

Dubai Residential Configuration Distribution – April-Mid May 2026

Configuration Distribution – What Buyers Are Choosing

The configuration mix in Q2 keeps returning to one central truth: Dubai’s residential market is still being carried by compact homes.

Studios and 1BR apartments continue to dominate transaction activity, not because they define the whole city’s housing need, but because they offer the easiest point of entry into Dubai’s property cycle.

They are smaller, more liquid, easier to rent, easier to resell, and better aligned with installment-led buying.

Configuration Mix: May 1–15 Snapshot

| Configuration | Transactions | Market Role |

| 1BR | 1,843 | Core liquidity segment |

| Studio | 1,337 | Entry investor product |

| 2BR | 941 | Balanced investor/end-user demand |

| 3BR | 210 | Family-led demand |

| 3BR+ | Limited | Lifestyle ballast |

The 1BR remains the most important unit type in the market. It sits at the intersection of affordability and livability.

For investors, it offers a wider tenant pool than studios.

For end-users, it still provides an attainable entry into newer Dubai communities.

For developers, it is the configuration that can absorb quickly without pushing the ticket size too high.

Studios perform a different function. Studios remain the most transaction-oriented product in the market. Their appeal lies in lower capital exposure, stronger rental yield potential, and faster absorption during launch cycles.

Together, studios and 1BR apartments remain the city’s liquidity engine.

Why Compact Homes Continue to Dominate

The dominance of compact homes is not accidental. It reflects the way Dubai’s residential market is currently financed and absorbed.

| Buyer Need | Why Compact Units Fit |

| Lower entry ticket | Smaller layouts reduce upfront exposure |

| Rental income | Strong demand from single professionals and young households |

| Payment-plan compatibility | Easier to absorb through staged payments |

| Resale liquidity | Larger buyer pool in the secondary market |

| Portfolio strategy | Investors can diversify across multiple units |

This is why compact apartments often outperform larger homes in transaction velocity, even when larger homes may offer better long-term livability.

The market is often rewarding accessibility as much as spatial scale.

The 2BR Segment Is the Bridge Market

The 2BR category continues to play a quieter but important role.

It does not move with the same speed as studios or 1BR homes, but it holds appeal across two buyer groups:

- investors looking for stronger tenant stickiness,

- and end-users seeking functional space without entering the high-ticket family-home segment.

In several mid-market corridors, the 2BR is becoming the bridge between investment logic and residential permanence.

It is where a buyer begins to ask a different question.

Not only:

“Will this rent well?”

But also:

“Can someone actually live here comfortably for several years?”

That shift matters because it separates short-cycle liquidity from deeper residential demand.

Larger Homes Remain Lower in Volume, But Strategically Important

The smaller transaction share of 3BR and 3BR+ homes should not be misread as weak demand.

Larger homes naturally transact more slowly because:

- tickets are higher,

- buyers take longer to decide,

- location sensitivity is greater,

- schools and commute patterns matter more,

- and rental yields are usually lower than compact units.

But they remain important because they provide lifestyle ballast to the market.

They are less speculative, more end-user driven, and more closely linked to long-term settlement.

This is especially relevant as Dubai continues attracting residents who are not only investing in the city, but choosing to live there for longer periods.

The Real Signal Is Not Size Alone

The configuration mix shows that Dubai’s market is not simply a story of small units versus large homes.

It is a story of buyer psychology.

Compact units reflect:

- liquidity,

- access,

- portfolio building,

- and rental yield.

Larger homes reflect:

- stability,

- family life,

- settlement,

- and lifestyle confidence.

Q2 confirms that liquidity is still winning the transaction count.

But the presence of steady 2BR and larger-home demand suggests that Dubai’s market is no longer only an investor marketplace. It is gradually becoming a more layered residential city, where different configurations speak to different life stages.

Unit Size Trends & Market Signals

One of the more revealing patterns in Q2 was not just what buyers purchased, but how much space they were willing to buy.

The data continues to show a market leaning toward efficient unit formats rather than expansive floor plates. This is particularly visible across emerging launch corridors where developers are optimizing layouts around affordability thresholds and payment-plan accessibility.

In many ways, Dubai’s apartment market now appears far more calibrated around efficiency than excess.

Not necessarily smaller living in the negative sense, but more calibrated living where:

- usable layouts matter more,

- entry ticket matters more,

- and the balance between affordability and functionality becomes more important.

The Market Continues to Favor Mid-Sized Apartments

The strongest concentration of activity remained within compact-to-mid-sized apartments.

| Unit Type | Typical Market Behavior |

| Compact Studios | Yield-focused investor demand |

| Efficient 1BRs | Highest liquidity |

| Mid-sized 2BRs | Lifestyle-investment crossover |

| Large 3BR+ Units | Lower velocity, higher stability |

Developers continue to appear to be designing around these transactional realities.

Across several active corridors, newer launches show:

- tighter planning efficiency,

- reduced circulation loss,

- more open-plan living areas,

- and layouts optimized around psychological pricing thresholds.

This is especially visible in projects targeting the AED 1M–2M ticket band.

📝 Interpretation

The market is gradually rewarding efficiency over sheer size.

That does not mean larger homes are disappearing. It means developers are becoming more strategic about where larger homes are introduced and how much inventory is allocated to them.

The Rise of the “Efficient Urban Home”

A noticeable Q2 trend is the growing normalization of apartments designed around urban practicality rather than excess space.

Several newer launches across:

- JVC,

- DLRC,

- Majan,

- and Madinat Al Mataar

reflect this shift clearly.

Common characteristics include:

- compact but functional kitchens,

- integrated dining-living layouts,

- reduced corridor wastage,

- flexible secondary rooms,

- and balcony-driven spatial extension.

These homes appear to be designed not just to look attractive in brochures, but to fit specific affordability mathematics.

That changes the architecture of the market itself.

🧭 AIQYA Insight

Dubai’s residential sector is gradually moving from a “size-driven” housing model toward an “efficiency-driven” housing model.

This mirrors patterns seen in several mature global cities where livability and affordability intersect through smarter planning rather than larger floor areas.

Larger Homes Are Becoming More Selective

While compact apartments dominate volume, larger residences continue to maintain a strong presence within:

- premium waterfront projects,

- villa communities,

- and upper-mid to luxury residential corridors.

However, the buyer profile for these homes is becoming more selective.

Larger units is beginning to depend on:

- long-term residency intent,

- family settlement,

- schooling ecosystems,

- lifestyle positioning,

- and wealth preservation.

This creates a slower but often more stable demand cycle.

Unlike compact apartments, larger homes are less influenced by rapid launch speculation and more influenced by confidence in long-term living conditions.

Space Is Now Being Valued Differently Across Segments

One of the most important structural shifts visible in Q2 is that space itself is no longer valued uniformly.

| Segment | What Buyers Prioritize |

| Investor-led compact homes | Yield, liquidity, entry pricing |

| Mid-market family apartments | Functionality & livability |

| Premium residences | Privacy, views, exclusivity |

| Ultra-prime homes | Scarcity & capital preservation |

This creates very different pricing dynamics across the city.

A compact apartment may achieve stronger transaction velocity and higher effective rental efficiency, while a larger residence may deliver stronger long-term residential stability despite slower turnover.

That distinction becomes important when interpreting:

- pricing trends,

- yield movement,

- and developer strategy.

The Psychological Threshold of Affordability

The strongest-performing projects during Q2 consistently aligned with one underlying principle: keeping units within psychologically accessible ticket sizes.

This is where unit sizing and payment planning become deeply interconnected.

A slight reduction in unit area can:

- reduce the entry ticket,

- improve installment affordability,

- widen the buyer pool,

- and accelerate launch absorption.

This is one reason why many newer launches appear highly calibrated rather than oversized.

Developers are no longer optimizing only for aspiration. Increasingly, they are designing for transaction conversion.

That subtle shift may become one of the defining characteristics of Dubai’s next residential cycle.

Top Projects & Developer Activity

Q2 2026 continued to demonstrate how strongly Dubai’s residential market now revolves around developer momentum.

Transaction activity across the quarter was not evenly distributed across the city. Instead, it clustered heavily around specific launches, phased releases, and high-absorption projects that aligned closely with the market’s current liquidity profile.

The result is a market shaped by developer sequencing rather than broad-based organic circulation.

Highest Activity Projects – May 1–15 Snapshot

| Project | Dominant Configuration Logic | Likely Buyer Orientation |

| Binghatti Skyflame | Compact 1BR-heavy inventory | Investor-led |

| DAMAC Lagoons Valencia | Larger suburban formats | Lifestyle & family |

| JVC Launches | Studio + 1BR mix | Yield-focused |

| The Wilds Residences | Lower-density premium layouts | Upper-mid end-user |

| Project | Transactions |

| Binghatti Skyflame 1 | 174 |

| Binghatti Skyflame 2 | 95 |

| DAMAC Lagoons – Valencia | 70 |

| The Wilds Residences | 63 |

| The Meriva Collection | 55 |

Several characteristics connect these projects despite differences in pricing and positioning.

Most align with at least one of the following:

- compact investor-led inventory,

- installment-driven accessibility,

- strong branding visibility,

- or location within expanding residential corridors.

Developers Are Shifting Toward Building for Absorption Velocity

One of the clearest Q2 signals is how precisely many launches now appear calibrated toward transaction conversion.

This is visible in:

- unit mix,

- payment-plan structures,

- launch pricing,

- and project phasing.

Rather than maximizing unit size, many developers now appear focused on optimizing:

- affordability thresholds,

- monthly payment perception,

- and investor entry flexibility.

📝 Interpretation

Dubai’s residential market rewards projects that can move inventory efficiently rather than simply position themselves as premium products.

This is especially true within:

- emerging apartment corridors,

- investor-heavy submarkets,

- and mid-ticket launch ecosystems.

Branding Is Becoming a Market Multiplier

Another notable shift visible during Q2 is the growing importance of developer branding within transaction behavior.

Certain developers now generate absorption momentum almost independent of broader market conditions because:

- launch familiarity reduces decision friction,

- payment-plan expectations are understood,

- and investor confidence becomes partially brand-driven.

This creates a layered hierarchy within the market where some launches attract immediate traction while others struggle despite similar pricing.

Developer branding now directly influences transaction velocity in certain segments. In several segments, it has effectively become a liquidity advantage.

The Return of the Launch Corridor

Several of the quarter’s most active projects were concentrated within what can often be described as launch corridors.

These are areas where:

- multiple developers operate simultaneously,

- inventory turnover remains high,

- and continuous release cycles sustain transactional momentum.

Among the strongest recurring zones:

- Majan,

- Dubai Land Residence Complex,

- JVC,

- and Madinat Al Mataar

continued showing elevated absorption.

| High-Activity Areas | Observed Market Role |

| Majan | Emerging mid-market launch cluster |

| DLRC | Investor-led compact housing |

| JVC | Mature liquidity ecosystem |

| Madinat Al Mataar | Expansion-driven growth corridor |

These locations has started to function as the operational core of Dubai’s apartment market.

Luxury Projects Continue to Shape Perception

At the opposite end of the spectrum, ultra-prime launches and branded residences continued generating some of the quarter’s highest-value benchmark transactions.

One of the largest apartment sales during the May 1–15 dataset crossed:

- AED 112M,

- at more than AED 7,300 psf.

Yet these transactions remain highly concentrated within a limited set of luxury products.

🧭 AIQYA Insight

There is now a widening separation between the projects that shape headlines and the projects that shape market volume.

Luxury developments often define perception. Compact apartment launches continue defining liquidity.

That dual structure here explains why Dubai can simultaneously appear:

- ultra-luxury driven internationally,

- while remaining fundamentally volume-led domestically.

Developer Strategy Is Becoming More Sophisticated

Q2 also reflected how developers are shifting toward adapting to buyer psychology rather than simply land economics.

Several broader strategic shifts are becoming visible:

- smaller but more efficient units,

- stronger launch sequencing,

- staggered inventory releases,

- psychologically attractive payment plans,

- and sharper ticket-size targeting.

This suggests a market moving into a more mature phase where developers compete not only through location and branding, but through transactional engineering itself.

The most successful projects are those that understand:

- how buyers calculate affordability,

- how investors evaluate liquidity,

- and how quickly the market absorbs specific configurations.

That may ultimately become one of the defining competitive advantages in Dubai’s next housing cycle.

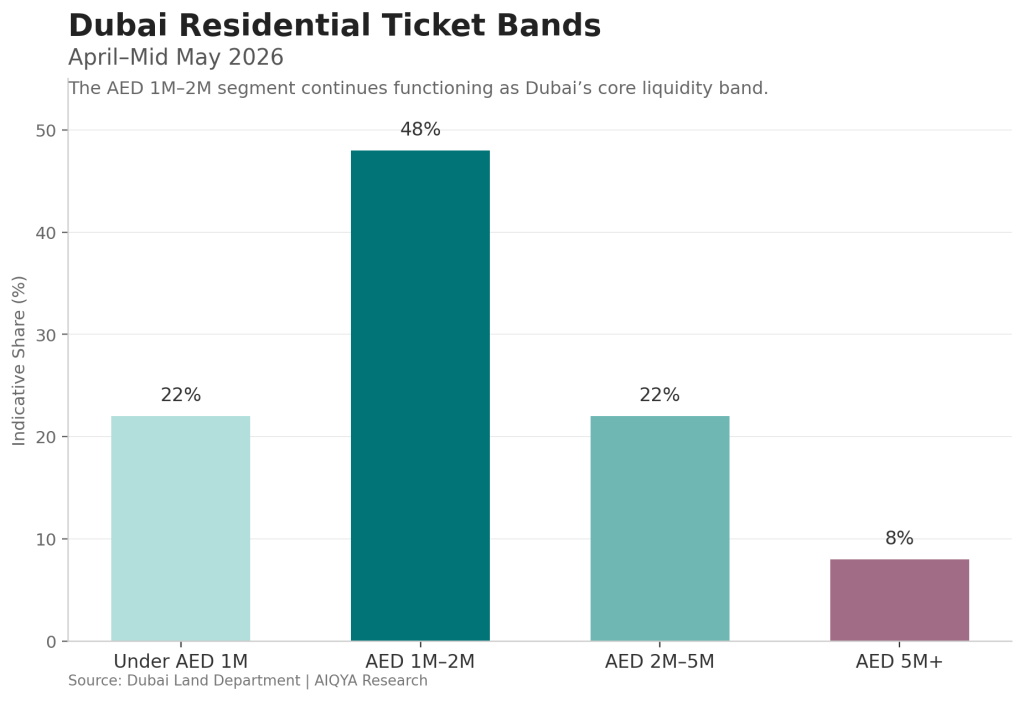

Dubai residential Ticket Bands – April-Mid May 2026

Affordability Snapshot – Where Buyers Are Spending

The centre of gravity in Dubai’s residential market remains firmly in the attainable investment band.

While ultra-prime transactions continue to draw attention, most of the market’s working liquidity is still concentrated around homes that sit within practical entry-ticket ranges. This is where the buyer pool is widest. It is also where payment plans, rental expectations, and resale confidence come together most efficiently.

The Core Spending Band

| Ticket Band | Market Meaning |

| Below AED 1M | Entry investor pool, studio-led activity |

| AED 1M–2M | Core liquidity band |

| AED 2M–5M | Upgrader and upper-mid market |

| AED 5M+ | Premium and luxury demand |

| AED 20M+ | Trophy capital, not broad-market signal |

The AED 1M–2M band continues to behave as the market’s most important liquidity zone.

It is large enough to include livable 1BR and some efficient 2BR inventory, but still accessible enough for investors entering through payment plans.

This is where Dubai’s property market feels most active, most competitive, and most structurally important.

Why the AED 1M–2M Band Matters

This price band is not simply a budget category. It has become a market mechanism.

It allows:

- investors to enter without excessive capital exposure,

- developers to maintain absorption speed,

- buyers to access newer communities,

- and rental yields to remain mathematically viable.

For many buyers, this band represents the point where aspiration and affordability still meet.

Below AED 1M, the market is highly yield-driven but often limited in terms of space and long-term end-user appeal.

Above AED 2M, buyer decisions become more deliberate, more location-sensitive, and more lifestyle-led.

The AED 1M–2M band sits between both worlds.

🧭 AIQYA Insight

This remains the city’s most functional investment band. It is not the most glamorous part of the market, but it is the part that keeps the transaction engine moving.

Affordability Is Beginning to Being Engineered

Developers are responding to affordability not only through pricing, but through design.

The stronger-performing projects increasingly show a combination of:

- efficient apartment sizes,

- staggered payment plans,

- compact unit mixes,

- and launch pricing aligned to psychological thresholds.

This is why unit size and ticket size must be read together.

A project may look expensive on a psf basis, yet remain liquid because the total ticket is still manageable.

That distinction is crucial in Dubai.

Buyers do not only respond to price per sqft. They respond to the monthly and staged payment burden.

The Luxury Market Is Real, But Not the Whole Story

Q2 recorded notable high-value transactions, including apartment sales above AED 100M.

These sales matter because they reveal Dubai’s continued appeal to global wealth. They also show the strength of branded, scarce, or waterfront inventory.

But they do not describe the market most buyers are participating in.

The broader market remains far more dependent on:

- compact homes,

- payment-plan absorption,

- mid-market corridors,

- and rental yield expectations.

This is where the difference between visibility and volume becomes important.

Luxury may shape perception, but affordability still drives participation.

A More Useful Way to Read Dubai’s Market

Instead of asking whether Dubai is becoming expensive or affordable as a whole, Q2 suggests a more useful question:

Where does each buyer still find a viable entry point?

For investors, that answer continues to sit in compact apartments and emerging corridors.

For end-users, affordability appears to depend on the trade-off between:

- location maturity,

- unit size,

- handover timeline,

- and payment structure.

For upgraders, the decision is becoming more selective, especially as larger homes require higher commitment and lower yield tolerance.

Dubai’s housing market remains accessible in parts, expensive in parts, and extremely selective at the top.

That mixed structure is not a contradiction. It is the market’s current form.

Continue Reading:

Supply, Yield & Dubai’s Next Housing Phase

The second part of this AIQYA market study explores rental trends, launch pipelines, developer activity, supply risks, and the next phase of Dubai’s residential cycle.

You may also like:

Dubai Residential Property Market April 2026 – What the Data Shows

Dubai Property Market Q1 2026: Structure, Pricing and Demand Trends