Dubai residential market February 2026 reveals a housing ecosystem driven by compact investor homes, strong off-plan activity, and steady mid-market demand. Beneath the headline numbers, a two-speed market is emerging where liquidity and long-term residential stability coexist.

- Key Highlights

- Market Overview

- Price Trends & Market Interpretation

- Primary vs Secondary Market Composition

- Configuration Distribution

- Unit Size Trends

- Top Projects by Transactions

- Affordability Snapshot

- Buyer Profile & Demand Lens

- Rental Trends & Yield Outlook

- Risks & Watchpoints

- Supply Snapshot – Where New Activity Is Emerging

- Final Observations & Buyer Takeaways

Key Highlights

1. February Maintains Strong Market Activity

Dubai recorded 12,082 apartment transactions in February 2026, continuing the strong transaction momentum seen across the residential market.

2. Transaction Value Crosses AED 25 Billion

Apartment sales generated AED 25.27 billion in transaction value, reflecting sustained buyer confidence across both investor and end-user segments.

3. Off-Plan Projects Continue to Dominate Sales

Off-plan properties accounted for the majority of transactions, highlighting the central role of new project launches in driving market liquidity.

4. The Mid-Market Segment Anchors Demand

With a median apartment ticket size of AED 1.39 million, the data suggests that the market’s core activity remains concentrated in the mid-price residential segment.

5. Prices Hold Firm Despite High Volumes

Median pricing remained around AED 1,744 per sq ft, indicating stable price levels even as transaction volumes remain elevated.

6. Smaller Homes Continue to Power Liquidity

Studios and one-bedroom apartments remain the most actively traded configurations, reflecting strong investor participation.

7. Larger Homes Reflect Residential Demand

Three-bedroom and larger apartments account for a smaller share of transactions, suggesting they are largely driven by long-term residential buyers rather than short-term investors.

8. A Dual-Speed Housing Market Is Emerging

The February data reinforces a broader pattern where compact apartments drive market velocity while larger homes support long-term residential demand.

The dominance of off-plan transactions shows how developer launch cycles remain the primary engine driving Dubai’s housing market.

Market Overview

Dubai’s residential market continues to move with remarkable velocity. February alone recorded 12,082 apartment transactions worth AED 25.27 billion, reinforcing a pattern that has become familiar across the past year: compact investment homes driving liquidity, while larger residences quietly anchor long-term residential demand.

Behind the headline numbers lies a market operating at two distinct speeds. Studios and one-bedroom apartments sustain transaction momentum, attracting investors drawn by rental yields and relatively accessible ticket sizes. At the same time, a smaller but steady stream of buyers continues to absorb larger homes in established communities, reflecting a quieter layer of end-user demand.

These purchases are less frequent but often reflect longer-term residential intent. The result is a market that operates at two distinct speeds. One layer is driven by liquidity and investor participation, while the other is shaped by residents choosing homes for lifestyle and permanence.

February’s numbers reinforce this dual structure. Compact units sustain the market’s velocity, while larger homes quietly anchor its stability. Together they form the underlying balance that continues to define Dubai’s residential ecosystem.

Core Market Metrics

| Metric | Value |

| Total Transactions | 12,082 |

| Total Transaction Value | AED 25.27 Billion |

| Median Price | AED 1,743.8 / sqft |

| Median Ticket Size | AED 1.39 Million |

| Off-plan Transactions | 8,844 |

| Ready Transactions | 3,238 |

Quick Reading of the Market

A few signals stand out immediately.

• Liquidity remains exceptionally strong, with more than twelve thousand apartment transactions in a single month.

• Off-plan projects dominate activity, accounting for nearly three quarters of sales.

• The median ticket size of AED 1.39M places the market firmly in the mid-segment, not the ultra-luxury bracket often associated with Dubai headlines.

• Prices remain firm, with the median price holding near AED 1,744 per square foot across active communities.

Taken together, these signals point to a market that remains deep, liquid, and heavily investor-oriented, but still supported by a base of genuine residential demand.

AIQYA Observation

What February reveals most clearly is not simply growth, but structure. Dubai’s residential market continues to be shaped by compact investment homes that keep transactions moving, while larger lifestyle apartments quietly provide long-term residential depth.

It is this balance, between velocity and stability, that continues to define the city’s housing market.

Price Trends & Market Interpretation

The February dataset suggests that price levels in Dubai’s residential market remain firm, supported by sustained investor demand and the continued dominance of off-plan project launches. The median apartment price for the month stands at AED 1,743.8 per square foot, indicating that pricing across the city’s active communities has held broadly stable.

At the same time, the transaction data reveals a clear divide between investment-oriented compact homes and larger lifestyle apartments. The two segments behave very differently in both pricing and transaction velocity.

Median Price Structure

| Metric | Value |

| Median Price | AED 1,743.8 / sqft |

| Median Ticket Size | AED 1.39 Million |

| Total Apartment Transactions | 12,082 |

The median ticket size of AED 1.39 million offers an important signal about the structure of the market. Despite frequent headlines about luxury real estate, the bulk of Dubai’s housing activity continues to occur in the mid-market investment band, where pricing remains accessible to international buyers and regional investors.

This middle layer continues to provide the core liquidity of the residential market.

What stands out in February’s data is not a sudden surge in pricing but rather its relative stability despite sustained transaction volumes. In markets where activity rises sharply, price volatility often follows. Dubai’s residential sector appears to be absorbing demand more evenly, partly because the off-plan pipeline continues to introduce new inventory at a steady pace.

Off-Plan vs Ready Price Dynamics

The price structure also reflects the strong influence of the off-plan market, which accounts for roughly 73% of apartment transactions.

Off-plan projects typically attract buyers through a combination of:

• competitive launch pricing

• staged payment plans during construction

• lower upfront capital requirements

These mechanisms allow investors to enter projects with relatively limited initial capital, which in turn sustains transaction velocity across new launches.

Ready properties, however, follow a different pricing logic. Their values tend to reflect:

• established community infrastructure

• proven rental income performance

• immediate occupancy value

As a result, the market effectively operates with two parallel price signals — one driven by developer launches and another shaped by the resale market in completed communities.

Compact Homes and Price Discovery

Studios and one-bedroom apartments play an outsized role in shaping monthly price benchmarks.

These units typically fall within the AED 700K to AED 1.5M range, and because they account for the largest share of transactions, they heavily influence metrics such as median price per square foot.

In effect, compact apartments act as the price discovery mechanism of the market. Their high transaction volumes allow the market to adjust quickly to shifts in investor demand.

Premium Segment Pricing

Larger homes tell a different story.

Three-bedroom apartments and larger residences typically exceed AED 4 million in ticket size, and premium branded residences in prime waterfront locations can reach substantially higher price levels.

These homes move more slowly through the market because buyers tend to be end-users rather than investors. Their decisions are influenced less by yield and more by factors such as:

• architectural quality

• community character

• proximity to lifestyle infrastructure

While they represent a smaller share of transactions, they contribute disproportionately to overall transaction value.

AIQYA Observation

Dubai’s residential pricing structure is best understood not as a single market, but as two overlapping layers.

Compact apartments form the liquidity layer, where pricing is shaped by investor activity and transaction velocity. Larger homes form the residential layer, where pricing reflects long-term lifestyle value rather than rapid turnover.

Both layers coexist, and together they define the broader rhythm of Dubai’s housing market.

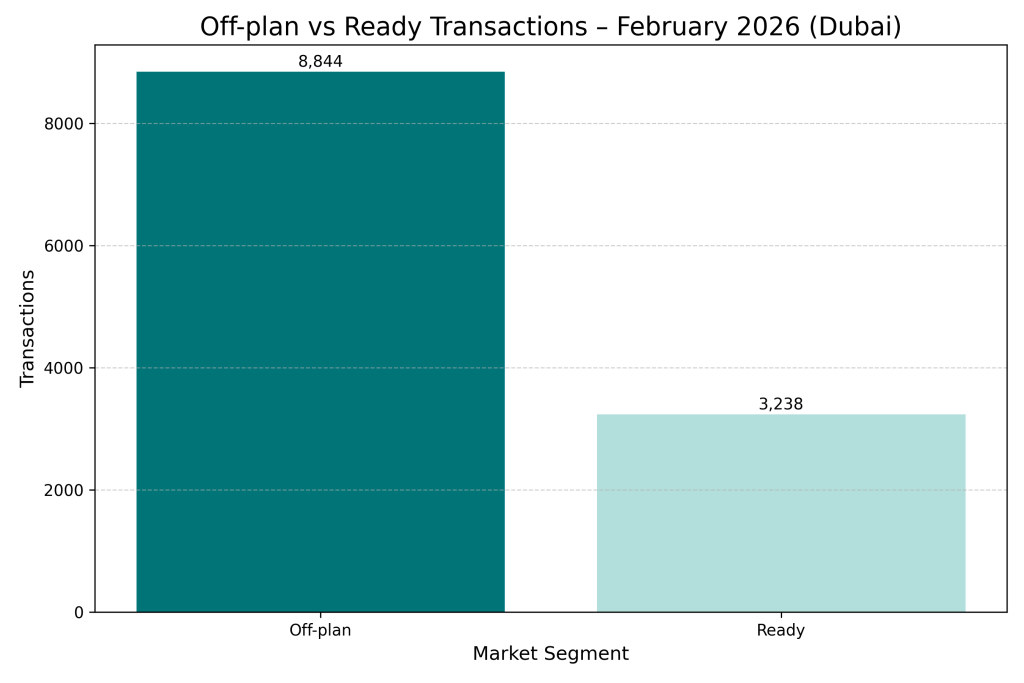

Primary vs Secondary Market Composition

Dubai’s residential market in February remained strongly oriented toward primary market activity, with new project launches continuing to drive the majority of transactions.

Of the 12,082 apartment sales recorded during the month, roughly 8,844 were off-plan purchases, while 3,238 involved ready properties in the secondary market. In percentage terms, this places the market split at 73% off-plan and 27% ready homes.

Transaction Split

| Market Segment | Transactions | Share |

| Primary Market (Off-plan) | 8,844 | 73% |

| Secondary Market (Ready) | 3,238 | 27% |

Developer-Led Momentum

The dominance of off-plan sales reflects a structural characteristic of Dubai’s housing market. Unlike many mature residential markets where resale activity dominates, Dubai’s growth cycle is often driven by new project launches.

Developers play a central role in sustaining market liquidity through:

• staged payment plans

• relatively low down payments

• global marketing reach

• launch-phase pricing strategies

These features make off-plan properties particularly attractive to international investors seeking capital appreciation during construction cycles.

The Role of the Secondary Market

Although smaller in volume, the resale market continues to provide an important stabilizing function.

Ready homes appeal to buyers who prioritize:

• immediate occupancy

• established neighborhoods

• proven rental demand

These transactions often involve end-users or long-term investors, which tends to produce more stable pricing dynamics in mature communities.

In many ways, the resale market acts as the structural backbone of the residential ecosystem, ensuring that completed developments continue to maintain long-term value.

AIQYA Observation

Dubai’s residential market operates through a clear dual structure.

The primary market provides the engine of growth, fueled by new launches and investor participation. The secondary market provides continuity, anchored by completed communities and longer-term residential ownership.

The health of the overall market depends on maintaining a balance between these two layers. When new supply is absorbed steadily, and resale markets remain active, the system tends to remain stable.

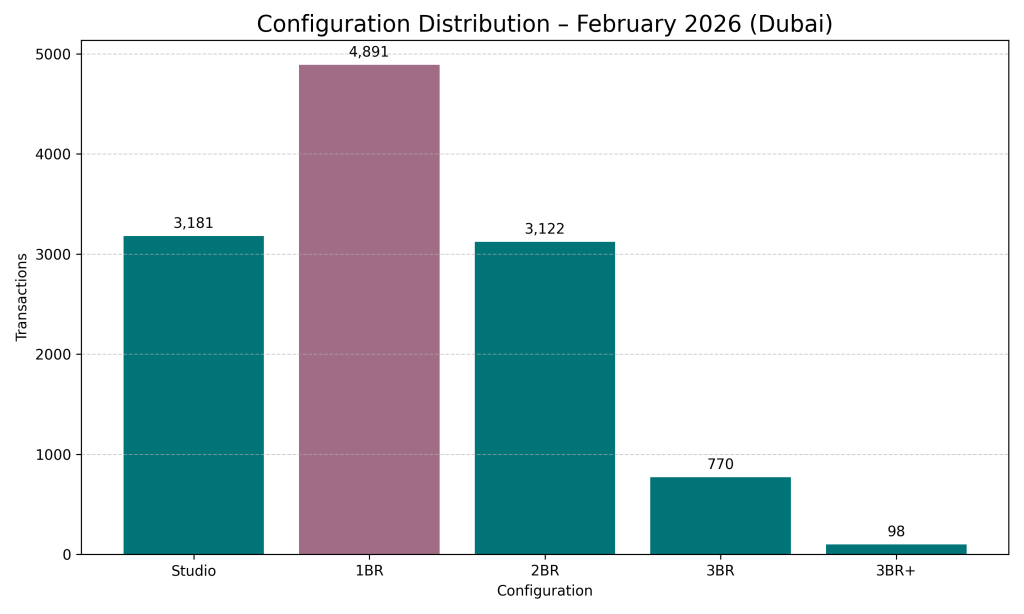

Configuration Distribution

The configuration mix of February’s transactions offers one of the clearest insights into how Dubai’s residential market actually functions. Of the 12,082 apartment transactions recorded during the month, the majority were concentrated in compact homes, particularly one-bedroom apartments and studios.

Together, these two categories account for more than two-thirds of all apartment sales, confirming the strong role of investor-oriented housing in shaping the city’s residential market.

February 2026 – Configuration Distribution

| Configuration | Transactions | Share |

| 1BR | 4,891 | 40.5% |

| Studio | 3,181 | 26.3% |

| 2BR | 3,122 | 25.8% |

| 3BR | 770 | 6.4% |

| 3BR+ | 98 | 0.8% |

| Unknown / Other | 20 | ~0.2% |

The Liquidity Engine

One-bedroom apartments clearly dominate the market, accounting for just over 40% of all transactions. Studios follow closely at around 26%.

Combined, these compact homes represent approximately 66% of total sales activity.

These units typically offer:

• lower entry ticket sizes

• higher rental yields

• faster resale turnover

As a result, they tend to attract investor participation rather than end-user buyers, particularly from international markets where Dubai property is viewed as a yield-generating asset.

This segment effectively forms the liquidity engine of the residential market, sustaining a high volume of transactions even during periods of market transition.

The Balanced Segment

Two-bedroom apartments represent roughly 26% of the market, forming a middle layer between investment homes and larger lifestyle properties.

This segment often attracts:

• small families relocating to Dubai

• long-term tenants upgrading homes

• investors seeking stable rental demand

Because of this mixed buyer base, two-bedroom apartments often show more balanced demand characteristics, combining elements of both investment activity and residential occupancy.

Lifestyle Homes

Larger homes — three-bedroom apartments and above — account for only about 7% of total transactions.

These homes are typically purchased by:

• long-term residents

• high-income professionals

• families seeking larger living spaces

Although they represent a smaller share of overall activity, they often command significantly higher ticket sizes and contribute meaningfully to the total value of residential transactions.

AIQYA Observation

The configuration distribution reinforces a pattern that has become characteristic of Dubai’s housing market.

Compact homes keep the market moving. Larger homes give it depth.

Studios and one-bedroom apartments provide transaction velocity, while larger homes reflect long-term residential demand. The two together create the layered structure that defines Dubai’s residential ecosystem.

Compact apartments sustain Dubai’s transaction velocity, while larger homes quietly anchor long-term residential demand.

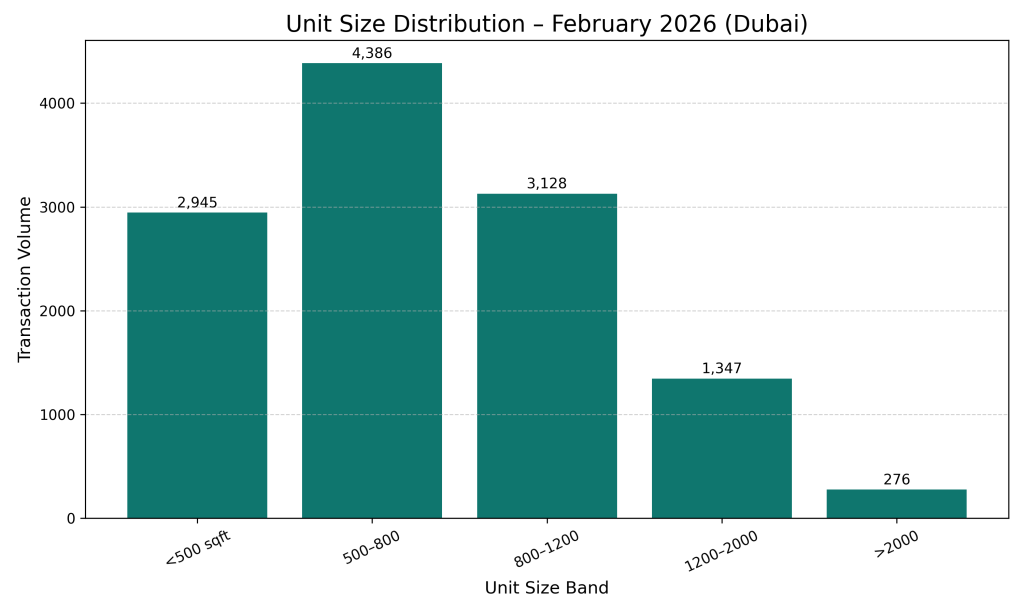

Unit Size Trends

The size distribution of apartments sold in February provides further insight into how Dubai’s residential market is structured. The median apartment size for the month stands at roughly 780 square feet, confirming the strong presence of compact, investor-oriented homes across new developments.

This aligns closely with the configuration distribution observed earlier, where studios and one-bedroom apartments dominate transaction activity.

February 2026 – Unit Size Distribution

| Size Band | Transactions | Share |

| Under 500 sqft | 2,945 | 24% |

| 500 – 800 sqft | 4,386 | 36% |

| 800 – 1,200 sqft | 3,128 | 26% |

| 1,200 – 2,000 sqft | 1,347 | 11% |

| Above 2,000 sqft | 276 | 2% |

Compact Homes Drive Liquidity

Nearly 60% of all apartment transactions fall below 800 square feet.

These units typically include:

• studios

• compact one-bedroom apartments

Their relatively small size keeps ticket prices accessible, which in turn makes them attractive to international investors and first-time buyers entering the Dubai market.

Because these units sell quickly and frequently, they also play a significant role in maintaining market liquidity and transaction velocity.

The Middle Layer of the Market

Apartments between 800 and 1,200 square feet account for roughly 26% of sales.

This segment largely consists of:

• larger one-bedroom apartments

• standard two-bedroom homes

These units often appeal to a mix of buyers. Investors still participate, but many purchases also come from long-term tenants or families seeking slightly larger living spaces.

This size range therefore forms a balanced layer of the market, where investment demand and residential demand intersect.

Large Homes Remain a Niche

Apartments larger than 1,200 square feet represent only about 13% of transactions, while homes above 2,000 square feet account for just 2% of sales.

These properties are typically associated with:

• three-bedroom apartments

• premium residences

• lifestyle-oriented developments

The smaller share of transactions reflects the fact that these homes are usually purchased by end-users rather than investors, which naturally results in lower transaction turnover.

AIQYA Observation

Dubai’s residential market is increasingly optimized around compact urban living.

Developers continue to prioritize smaller homes because they lower entry price barriers and help projects achieve faster sales absorption. Larger apartments remain an important part of the residential ecosystem, but they occupy a much smaller portion of the transaction landscape.

In essence, the city’s housing market is designed around high-liquidity compact homes supported by a smaller layer of lifestyle residences.

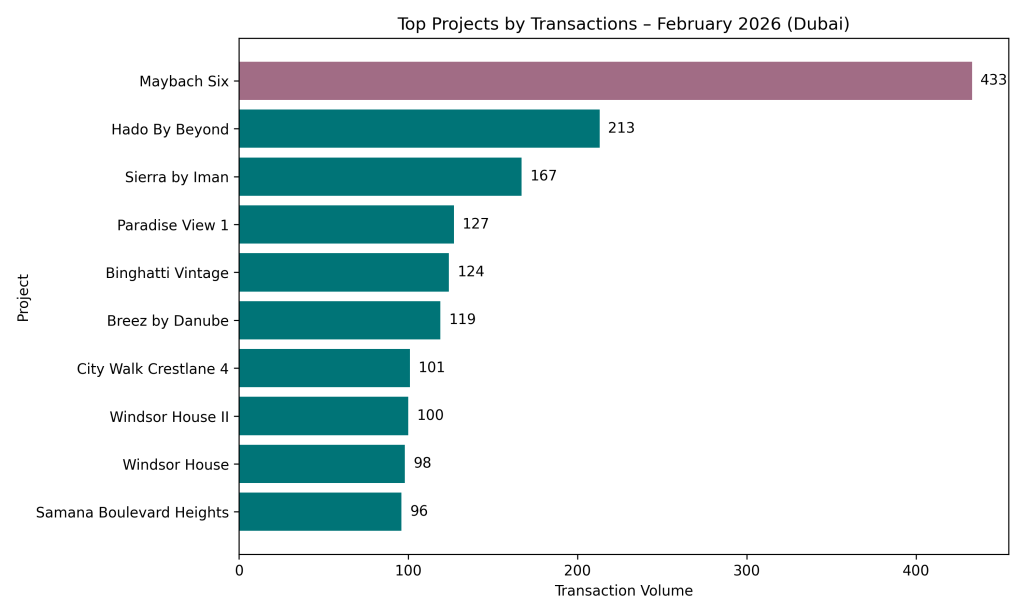

Top Projects by Transactions

Transaction data for February highlights the projects that generated the highest sales activity during the month. These developments offer an important window into how the market is absorbing new supply, particularly in the off-plan segment where most transactions are concentrated.

A closer look at the rankings reveals two distinct clusters:

projects positioned for high-volume investor demand, and a smaller group of premium lifestyle developments commanding higher ticket values.

The projects ranking highest in February transactions offer a useful lens into how new supply is being absorbed across different price tiers and developer strategies.

February 2026 – Top Projects by Transactions

| Rank | Project | Transactions | Median Price (AED/sqft) | Median Ticket |

| 1 | Maybach Six | 433 | 3,622 | 1.40M |

| 2 | Hado By Beyond | 213 | 3,177 | 2.77M |

| 3 | Sierra by Iman | 167 | 1,675 | 1.32M |

| 4 | Paradise View 1 | 127 | 893 | 720K |

| 5 | Binghatti Vintage | 124 | 1,841 | 691K |

| 6 | Breez by Danube | 119 | 3,452 | 1.51M |

| 7 | City Walk Crestlane 4 | 101 | 3,346 | 3.99M |

| 8 | Windsor House II | 100 | 1,547 | 1.35M |

| 9 | Windsor House | 98 | 1,455 | 1.56M |

| 10 | Samana Boulevard Heights | 96 | 1,664 | 758K |

Developer-Led Off-Plan Momentum

Several of the projects at the top of the table are recent off-plan launches, which explains the high number of transactions recorded within a relatively short period.

Developers such as:

• Binghatti

• Danube

• Samana

• Iman Developers

continue to dominate high-volume investor-focused segments.

These projects typically share several characteristics:

• compact unit mixes

• accessible entry prices

• flexible payment plans

• strong marketing exposure

Such features make them well-suited for investors seeking liquidity and rental potential, which helps drive rapid early-stage sales.

Mid-Market Liquidity vs Premium Lifestyle

The transaction rankings also reveal a clear contrast between liquidity-driven projects and higher-value developments.

Investor-Focused Liquidity Projects

Paradise View 1

Samana Boulevard Heights

Binghatti Vintage

Typical ticket sizes:

AED 700K – AED 1.3M

These projects generate high transaction velocity, largely due to their accessibility to international investors.

Premium Lifestyle Projects

City Walk Crestlane

Maybach Six

Hado By Beyond

Typical ticket sizes:

AED 2M – AED 4M+

These developments record fewer buyers relative to the broader market but contribute significantly to overall transaction value and pricing benchmarks.

AIQYA Observation

The transaction leaders for February reinforce a familiar pattern in Dubai’s residential market.

Projects that combine compact layouts, investor-friendly pricing, and flexible payment plans tend to dominate sales rankings. Premium developments may command higher prices, but liquidity in the market still gravitates toward accessibility rather than luxury.

Affordability Snapshot

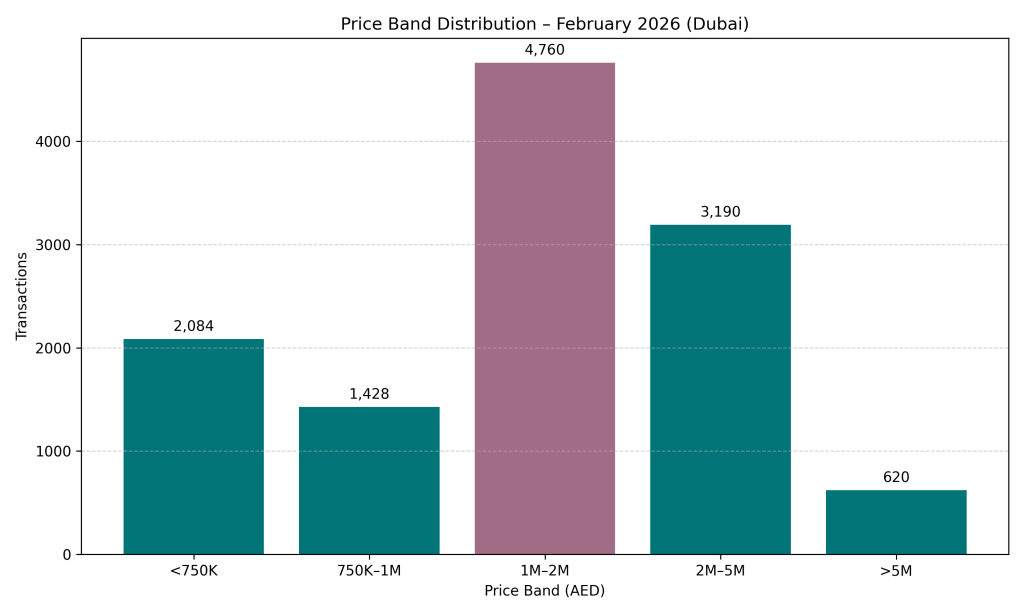

Looking at the distribution of transaction values provides a clearer picture of where most buyers are actually participating in the market. While Dubai often attracts attention for its luxury developments, the February transaction data shows that the majority of residential activity continues to take place within the mid-market affordability range.

Of the 12,082 apartment transactions recorded during the month, nearly 40% fall within the AED 1M to AED 2M price band, making it the most active segment of the residential market.

February 2026 – Price Band Distribution

| Price Band | Transactions | Share |

| Under AED 750K | 2,084 | 17.2% |

| AED 750K – 1M | 1,428 | 11.8% |

| AED 1M – 2M | 4,760 | 39.4% |

| AED 2M – 5M | 3,190 | 26.4% |

| Above AED 5M | 620 | 5.1% |

The Core Buying Zone

The AED 1M – 2M range clearly emerges as the center of gravity for Dubai’s residential market.

Homes within this band typically include:

• mid-sized one-bedroom apartments

• compact two-bedroom homes

• investor-focused developments in emerging communities

This price level strikes a balance between affordability and rental income potential, making it particularly attractive to both local and international buyers.

Entry-Level Investment Layer

Properties priced below AED 1 million still account for a meaningful portion of activity.

Combined, the segments below AED 1M represent roughly 29% of all transactions.

These homes are typically:

• studio apartments

• compact one-bedroom units

• developments in emerging suburban districts

Buyers in this segment often include first-time overseas investors or those targeting short-term rental opportunities.

Upper Mid-Market Segment

Homes priced between AED 2M and AED 5M account for about 26% of the market.

This segment typically includes:

• larger two-bedroom apartments

• three-bedroom homes

• properties located in established communities

Buyers here tend to include a mix of end-users and longer-term investors, reflecting a shift away from purely yield-driven purchases.

Luxury Market

Transactions above AED 5 million represent only about 5% of total sales.

These homes include:

• branded residences

• waterfront apartments

• prime lifestyle developments

Although small in volume, they contribute significantly to the overall value of residential transactions, reflecting Dubai’s continued role as a global luxury property destination.

AIQYA Observation

Dubai’s residential market continues to orbit around a mid-market affordability anchor.

Compact homes sustain transaction velocity at the lower end of the market, while premium lifestyle residences command higher prices but represent a smaller share of total activity. The AED 1M–2M range therefore, acts as the market’s gravitational center, balancing accessibility, investment demand, and residential appeal.

Buyer Profile & Demand Lens

The transaction patterns observed in February suggest that Dubai’s residential market is being shaped by three distinct buyer profiles, each operating within different price and configuration segments. Rather than a single homogeneous market, the data points to a layered ecosystem where investors, long-term residents, and lifestyle buyers interact in different ways.

Understanding these groups is important because each one influences how projects are designed, priced, and absorbed by the market.

The Investor Segment

The Market’s Liquidity Engine

The most active segment of buyers remains concentrated in studios and one-bedroom apartments, which together account for roughly two-thirds of all transactions.

These homes typically fall within the AED 750K to AED 1.5M range, aligning closely with the affordability band identified earlier as the market’s core.

Investor motivations in this segment generally include:

• rental yield potential

• short-term rental flexibility

• relatively low entry ticket sizes

• developer payment plans that reduce upfront capital requirements

Many of the projects appearing in the Top Projects rankings are designed precisely for this audience, offering compact layouts and aggressive marketing aimed at international buyers.

In practical terms, this segment forms the transaction backbone of Dubai’s residential market, sustaining liquidity even during periods of broader market adjustment.

The Balanced Ownership Segment

Stability Through Residential Demand

Two-bedroom apartments represent roughly one quarter of the market, forming a more balanced segment between investors and end-users.

Buyers in this category often include:

• young families relocating to Dubai

• long-term expatriate residents

• investors seeking stable, longer-term rental income

These homes typically fall within the AED 1.5M to AED 3M range, placing them slightly above the entry-level investment layer but still within reach for many professional households.

Compared with compact units, two-bedroom homes tend to experience:

• lower resale turnover

• longer tenancy durations

• stronger end-user ownership

As a result, this segment contributes an important layer of stability to the residential ecosystem, particularly within established communities.

The Lifestyle Buyer Segment

Space, Location, and Long-Term Living

Larger apartments — particularly three-bedroom homes and above — account for only a small share of total transactions but represent a different kind of demand.

Typical buyers in this segment include:

• established expatriate families

• senior professionals relocating to Dubai

• international buyers seeking premium lifestyle residences

Ticket sizes in this category often exceed AED 3M and can rise significantly higher in branded or waterfront developments.

Unlike investor-driven purchases, these buyers are typically motivated by:

• larger living spaces

• community character

• proximity to lifestyle infrastructure such as schools, parks, and waterfront districts

Although fewer in number, these purchases contribute meaningfully to overall market value.

AIQYA Observation

The data reinforces the idea that Dubai’s residential market operates as a two-speed ecosystem.

Compact apartments maintain transaction velocity through investor participation, while larger homes provide a quieter but important layer of long-term residential stability.

Both groups are essential. Investors keep the market liquid, while residents give it permanence.

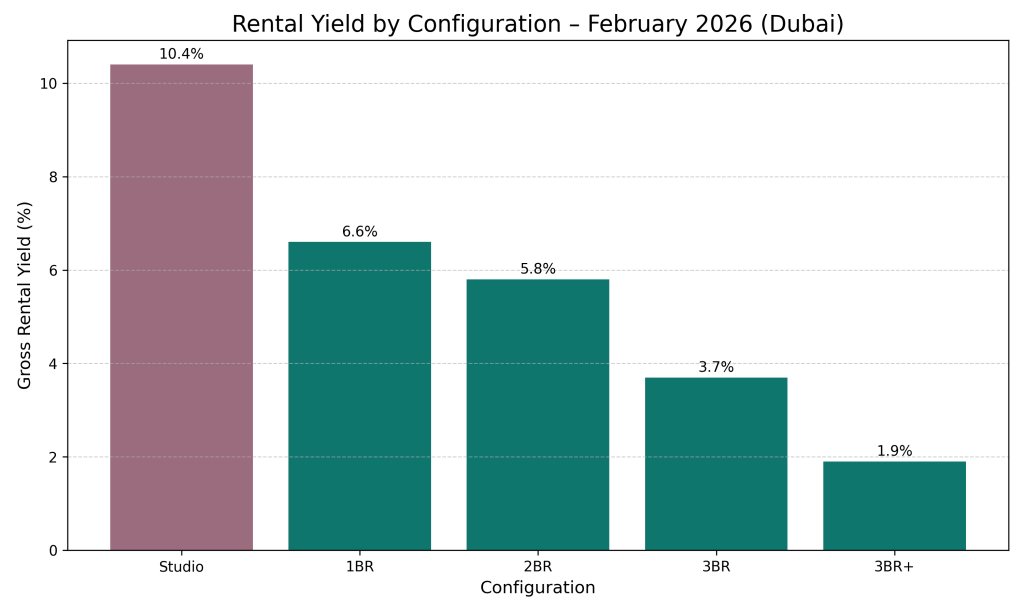

Rental Trends & Yield Outlook

Rental performance remains one of the strongest underlying drivers of Dubai’s residential investment market. By combining the Ejari rental dataset of 47,821 registered residential lease contracts with the February apartment sales data, it becomes possible to estimate the gross rental yield profile across different configurations.

The results reveal a clear pattern: smaller homes generate significantly higher rental returns, while larger lifestyle apartments show lower yields due to their higher capital values.

Median Annual Rent by Configuration

| Configuration | Median Annual Rent |

| Studio | AED 75,000 |

| 1BR | AED 85,000 |

| 2BR | AED 140,000 |

| 3BR | AED 155,000 |

| 3BR+ | AED 240,000 |

Estimated Gross Rental Yields

| Configuration | Median Ticket | Median Rent | Gross Yield |

| Studio | 724K | 75K | 10.4% |

| 1BR | 1.29M | 85K | 6.6% |

| 2BR | 2.40M | 140K | 5.8% |

| 3BR | 4.17M | 155K | 3.7% |

| 3BR+ | 12.76M | 240K | 1.9% |

Yield Compression with Size

One of the clearest trends visible in the data is the yield gradient across apartment sizes.

Compact units generate significantly stronger returns:

• Studios approach 10% gross yields

• One-bedroom apartments deliver roughly 6–7%

• Two-bedroom homes remain near 5–6%

As unit sizes increase, rental yields decline because property prices rise faster than rental income.

The Investor Sweet Spot

The one-bedroom segment appears to offer the most balanced investment profile.

It combines:

• moderate purchase price

• strong tenant demand

• stable rental income

This helps explain why 1BR units represent the single largest configuration in the February transaction dataset, accounting for over 40% of apartment sales.

Lifestyle Homes and Yield Trade-Offs

Larger apartments show a different economic profile. While they command significantly higher ticket values, their rental yields tend to fall below 4%.

Buyers in this segment are therefore less likely to prioritize rental income. Instead, purchases are often driven by lifestyle considerations such as space, location, and long-term residential use.

For these buyers, the investment thesis often centers more on capital appreciation and quality of living than on rental yield alone.

AIQYA Observation

Dubai’s residential investment market continues to be strongly supported by yield-efficient compact homes.

Studios and one-bedroom apartments function as the market’s core investment assets, offering relatively high rental returns alongside strong resale liquidity. Larger homes follow a different logic altogether, acting more as lifestyle residences than yield-driven investments.

The coexistence of these two segments continues to shape the structure of Dubai’s housing market.

Risks & Watchpoints

February’s numbers point to a market that remains active, liquid, and broadly confident. Yet strong transaction momentum should not be mistaken for the absence of risk. Dubai’s residential market has always been dynamic, and that dynamism is part of its appeal. It is also what makes the market sensitive to shifts in sentiment, supply, and global capital flows.

The key watchpoints at this stage are less about immediate weakness and more about how sustainable the current pace of activity remains.

1. Dependence on Off-Plan Liquidity

The most obvious structural feature of the February market is its reliance on the off-plan segment. With 73% of apartment transactions taking place in new launches, developers remain central to market momentum.

This creates depth and visibility, but it also introduces a degree of fragility. Off-plan markets are highly responsive to sentiment. If investor confidence softens, or if financing conditions become less accommodating, absorption can slow faster than in completed communities.

In such phases, the response is often familiar:

• extended payment plans

• launch incentives

• price adjustments through offers rather than headline cuts

None of these signals distresses by itself, but it is the first place where a cooling market usually reveals itself.

2. Concentration in Compact Units

Studios and one-bedroom apartments account for roughly two-thirds of apartment transactions, which tells us where liquidity currently sits. It also hints at where future competition may emerge.

Developers continue to favor compact layouts because they:

• keep ticket sizes accessible

• improve launch absorption

• align with investor demand

But when too much supply is concentrated in similar unit types within the same micro-markets, the result can be localized pressure on rents, resale premiums, and occupancy performance.

The risk here is not citywide oversupply in the abstract. It is micro-market crowding, especially in districts where several investor-led projects are scheduled to be completed within a short window.

3. Yield Compression in Larger Homes

The yield profile becomes materially weaker as unit sizes increase. Studios and one-bedroom apartments remain attractive from an income perspective, but three-bedroom and larger homes show a much sharper compression in returns.

This matters because higher-value inventory can become harder to justify for investors if:

• rental growth slows

• purchase prices keep rising

• competing premium projects continue to launch nearby

Larger homes will still attract end-users, but their appeal to investment buyers becomes narrower unless supported by strong scarcity, location quality, or long-term appreciation potential.

4. Sensitivity to Global Capital Flows

Dubai’s residential market is deeply connected to international investor capital. That has been one of its great strengths, but it is also a variable that sits outside the city’s direct control.

Changes in:

• global interest rates

• currency movements

• geopolitical tensions

• tax or regulatory shifts in source markets

can influence buyer appetite, especially in the compact, investor-driven segments that currently dominate transaction volumes.

In other words, Dubai may be local in geography, but its residential demand is often global in origin.

5. Speed of the Development Cycle

Dubai’s development ecosystem moves quickly. When demand is strong, supply responds fast. That responsiveness is part of the city’s development culture, and it often prevents the kind of prolonged shortages seen elsewhere.

Still, rapid response also means the market requires careful observation. If launch activity rises faster than end demand can absorb over time, pricing pressure can emerge first in:

• investor-dense communities

• projects with similar product mix

• locations where infrastructure maturity is still catching up with supply

The real question is not whether supply is growing. It almost always is. The more important question is whether supply is arriving in the right places, in the right formats, and at the right speed.

AIQYA Observation

Dubai’s residential market remains fundamentally strong, but it is also highly responsive. That responsiveness is a strength when demand is rising, and a vulnerability when sentiment turns.

For buyers and investors, the most useful watchpoints in the coming quarters are clear:

• the pace of off-plan launches

• rental performance in compact-unit corridors

• resale liquidity in completed communities

• the depth of demand beyond investor-led buying

The healthiest projects are likely to be those that can perform not only as financial products, but also as places people genuinely want to live in.

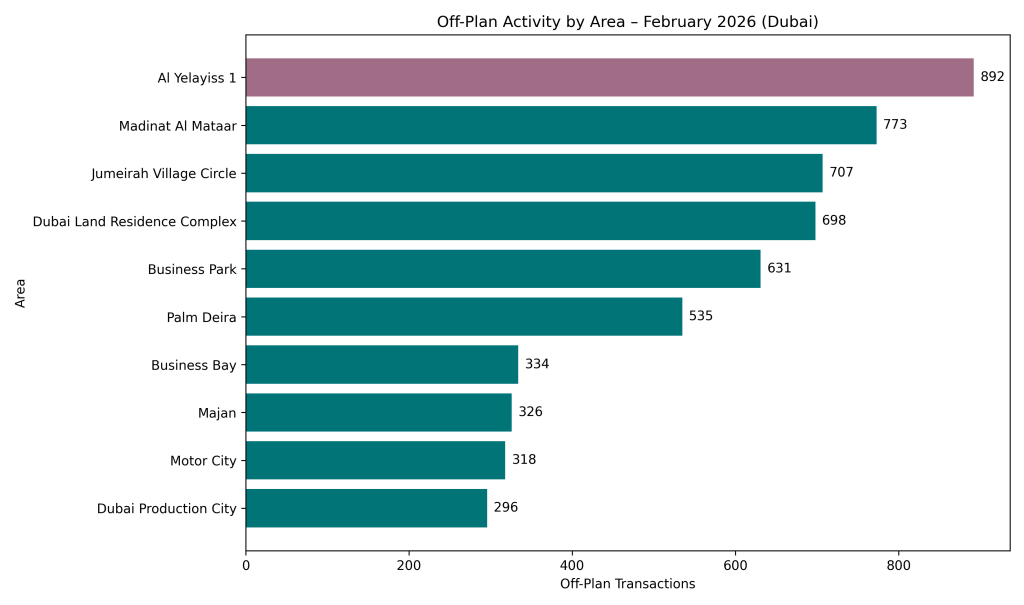

Supply Snapshot – Where New Activity Is Emerging

One of the defining characteristics of Dubai’s residential market is the speed at which supply responds to demand. When investor appetite rises, developers tend to move quickly, releasing new phases and projects across multiple districts.

February’s off-plan transaction data provides a useful glimpse into where the next wave of residential supply is concentrating. Because off-plan purchases represent homes that are still under construction or recently launched, they act as a reliable proxy for future inventory entering the market.

The patterns emerging from the data suggest that the next cycle of supply is not concentrated in traditional luxury districts, but rather in mid-market communities where compact apartments remain in strong demand.

Off-Plan Activity by Area

| Rank | Area | Off-plan Transactions |

| 1 | Al Yelayiss 1 | 892 |

| 2 | Madinat Al Mataar | 773 |

| 3 | Jumeirah Village Circle | 707 |

| 4 | Dubai Land Residence Complex | 698 |

| 5 | Business Park | 631 |

| 6 | Palm Deira | 535 |

| 7 | Business Bay | 334 |

| 8 | Majan | 326 |

| 9 | Motor City | 318 |

| 10 | Dubai Production City | 296 |

Emerging Mid-Market Corridors

Several of the areas appearing at the top of the list share similar characteristics. They are locations where developers can still introduce projects with accessible entry prices and relatively compact apartment formats.

Districts such as:

• Jumeirah Village Circle

• Dubai Land Residence Complex

• Majan

• Dubai Production City

have gradually evolved into high-absorption corridors for investor-oriented developments.

These communities often attract buyers seeking:

• lower entry ticket sizes

• strong rental demand

• proximity to growing infrastructure networks

For developers, they offer the combination of affordable land costs and strong investor appetite, making them ideal locations for high-volume residential launches.

Infill Development in Mature Districts

Alongside these emerging corridors, some established districts continue to see selective infill development.

Business Bay, for instance, still appears prominently in off-plan activity despite being one of the city’s more mature residential areas. In such locations, new projects tend to focus on premium positioning, architectural design, and lifestyle branding rather than purely on price accessibility.

This creates a two-tier development landscape where:

• emerging districts drive transaction volume

• mature districts capture higher-value projects

Projects Driving New Supply

| Rank | Project | Off-plan Transactions |

| 1 | Maybach Six | 436 |

| 2 | Hado By Beyond | 213 |

| 3 | Sierra by Iman | 167 |

| 4 | Damac Islands 2 – Bahamas 1 | 139 |

| 5 | Damac Islands 2 – Bahamas 2 | 126 |

| 6 | Binghatti Vintage | 124 |

| 7 | Shahrukhz by Danube | 124 |

| 8 | Damac Islands 2 – Maui | 120 |

| 9 | Breez by Danube | 119 |

| 10 | Damac Islands 2 – Cuba | 111 |

These projects highlight the continued presence of high-volume mid-market developers, particularly those focused on investor-led product formats.

Developers such as:

• Danube

• Binghatti

• Iman

• DAMAC

continue to shape the next phase of supply through projects built around compact apartments and flexible payment plans.

AIQYA Observation

Dubai’s supply pipeline remains closely aligned with the structure of demand. As long as investor participation continues to favor compact, mid-ticket homes, developers are likely to concentrate their launches in districts where these formats can be delivered efficiently.

In this sense, supply is not expanding randomly. It is expanding precisely where the market is currently most liquid.

Final Observations & Buyer Takeaways

Dubai’s residential market in February 2026 continues to display the characteristics that have defined its recent cycle: strong transaction liquidity, a dominant off-plan segment, and a clear preference for compact apartment formats.

Behind the headline transaction volumes lies a market that is functioning in two distinct layers.

The first layer is driven by investor-led demand. Studios and one-bedroom apartments form the backbone of transaction activity, supported by relatively accessible entry prices and rental yields that remain attractive by global standards. These homes act as the market’s liquidity engine, changing hands frequently and sustaining a steady stream of new launches across emerging residential districts.

The second layer moves at a different pace. Larger apartments and lifestyle-oriented residences trade less frequently, but they attract buyers seeking space, stability, and long-term residence. These homes function as the market’s lifestyle ballast, anchoring communities even as investor-led segments move more quickly.

This dual structure has become one of Dubai’s defining real estate characteristics. A city capable of accommodating both global investors seeking yield and long-term residents looking for quality of life.

Several key takeaways emerge from the February data:

1. Compact homes remain the market’s liquidity core.

Studios and one-bedroom apartments account for the majority of transactions, reflecting both investor demand and developer product strategy.

2. Off-plan launches continue to shape market momentum.

New developments represent the majority of transactions, confirming that developers remain central to the city’s residential expansion.

3. Rental yields continue to support investment demand.

Strong rental performance, particularly in smaller units, reinforces Dubai’s appeal as an income-generating real estate market.

4. Larger homes follow a different investment logic.

While their rental yields are lower, these properties attract buyers prioritizing lifestyle, long-term residence, and community stability.

For buyers and investors, the most important lesson may be a simple one. Dubai is not a single market moving in one direction. It is a layered ecosystem of different housing products, buyer motivations, and investment horizons.

Understanding where a property sits within that ecosystem often matters more than simply tracking price movements.

In that sense, the February market does not merely reveal how many homes were sold. It reveals how the city itself is evolving, one transaction at a time.

Data Source & Method Note

Figures in this report are based on Dubai Land Department (DLD) registered transactions for February 2026, covering residential freehold apartment sales. Price metrics are derived using the median price per square foot calculated from transaction value divided by registered area.

Rental yield estimates are based on Ejari lease registrations for the same period.

Figures are based on official registered datasets. Minor gaps may exist due to naming inconsistencies or exclusions. This report is intended for insight and education, not financial advice.

It is important to note that the February transaction data captured in this report reflects market activity prior to the geopolitical escalation in the region that began unfolding in early March. While Dubai’s residential market has historically demonstrated resilience during periods of regional uncertainty, the coming months will offer clearer insight into how investor sentiment and cross-border capital flows respond to the evolving geopolitical landscape.