Contents

- Puppalguda Market Overview Q2 2025

- Key Market Metrics – Q1 vs Q2 2025

- Price Trends & Market Interpretation

- Resale vs Developer Sales – Market Composition

- Configuration Distribution – What Are Buyers Choosing?

- Unit Size Trends & Market Signals

- Top Projects & Developer Activity – Who’s Leading Sales?

- Affordability Snapshot – Where Buyers Are Spending

- Buyer Profile & Demand Lens

- Rental Trends & Yield Outlook

- Configuration Spotlight – Project-Wise Breakdown

- Risks & Watchpoints

- Supply Snapshot – What’s in the Pipeline?

- Final Observations & Buyer Takeaways

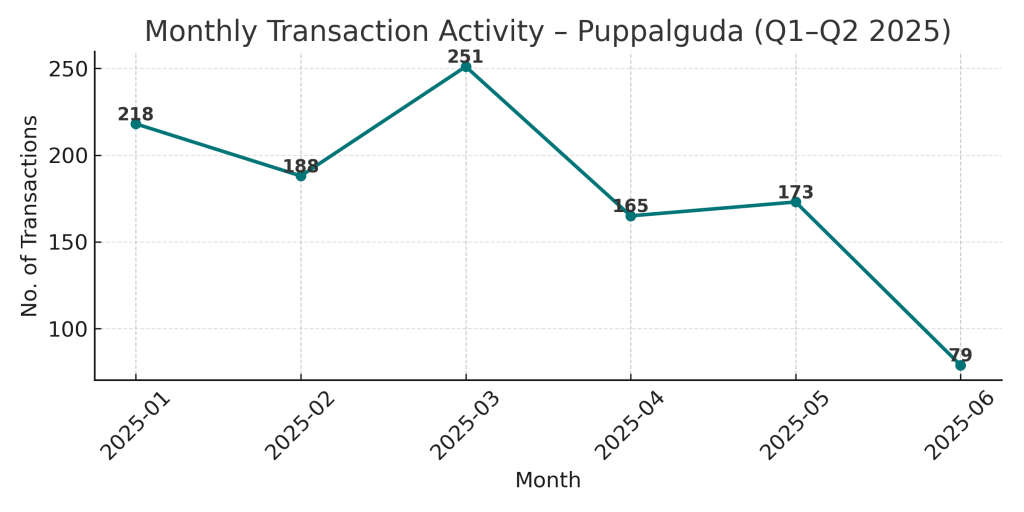

Puppalguda Market Overview Q2 2025

Puppalguda real estate continued its steady evolution in Q2 2025, attracting end-users priced out of Kokapet and Narsingi but still seeking gated community living. With most sales concentrated in mid-sized 3 BHKs under ₹1.2 Cr, Puppalguda now appeals to families prioritizing usable space over brand premiums. The market remains absorption-led, with moderate pricing growth and strong preference for nearing-possession inventory. For many, Puppalguda strikes the right balance between accessibility, community scale, and long-term usability.

Key Market Metrics – Q1 vs Q2 2025

Exclusive Research. Structured Access.

To preserve quality and purpose,

AIQYA’s research is shared by request.

Already part of AIQYA Access?Sign In