- Market Overview – Nallagandla Q2 2025

- Key Market Metrics – Q1 vs Q2 2025

- Price Trends & Market Interpretation

- Resale vs Developer Sales – Market Composition

- Configuration Distribution – What Are Buyers Choosing?

- Unit Size Trends & Market Signals

- Top Projects & Developer Activity – Who’s Leading Sales?

- Affordability Snapshot – Where Buyers Are Spending

- Buyer Profile & Demand Lens

- Rental Trends & Yield Outlook

- Configuration Spotlight – Project-Wise Breakdown

- Risks & Watchpoints

- Supply Snapshot – What’s in the Pipeline?

- Final Observations & Buyer Takeaways

Market Overview – Nallagandla Q2 2025

Nallagandla Real Estate continues to demonstrate its staying power as a mature, mid-premium residential hub within Hyderabad’s western corridor. While the overall transaction count declined by ~19% in Q2 2025, the underlying market dynamics signal consolidation rather than slowdown. With a higher resale share, rising median prices, and sustained demand for 3 BHK formats, the micro-market is quietly shifting gears — from a new-launch-led destination to a self-sustaining, end-user–focused ecosystem.

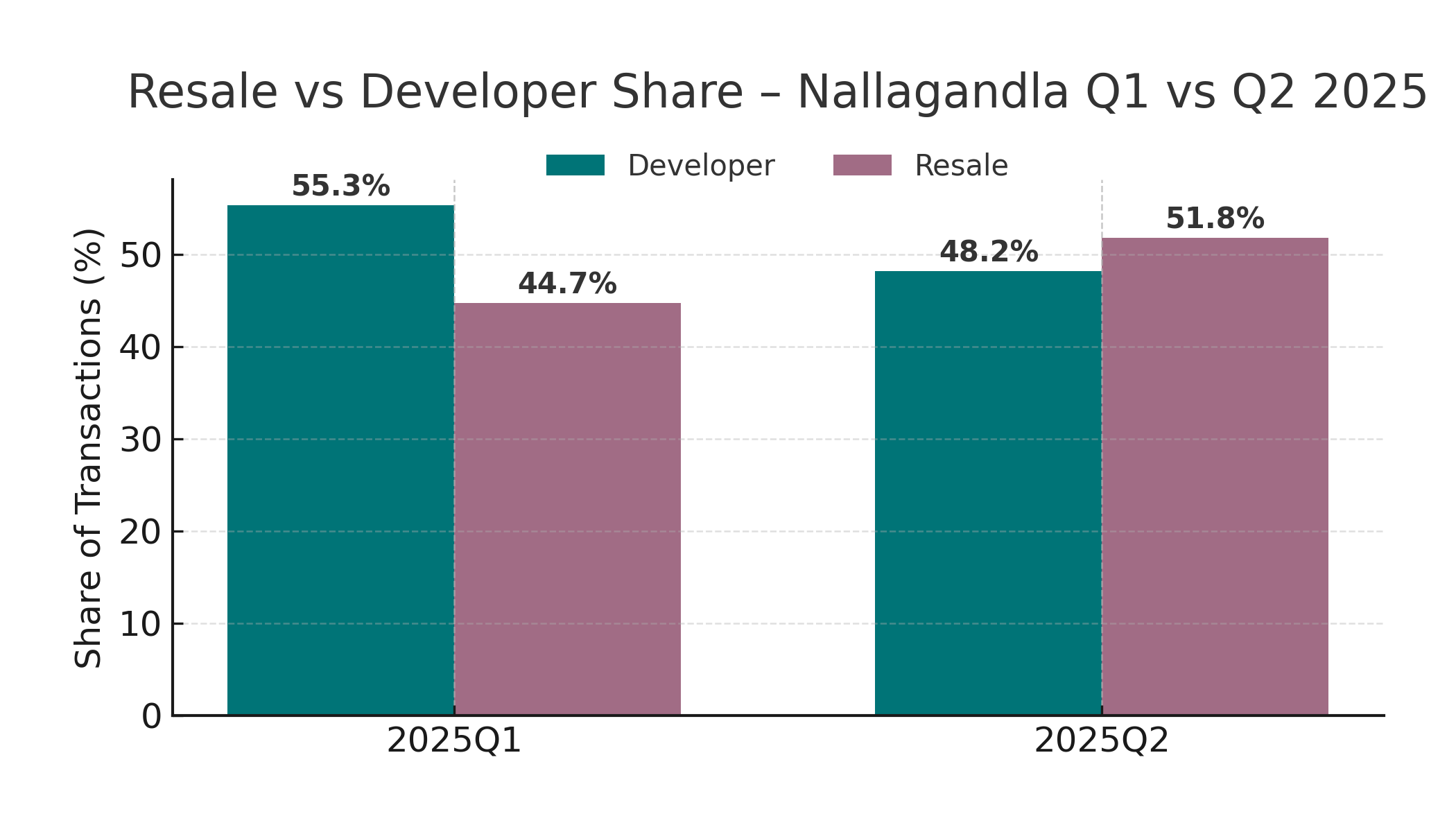

A notable 51.8% of all transactions in Q2 came from resale deals — a significant uptick from 44.7% in Q1. This suggests a deepening of the secondary market, especially in well-established gated communities like Aparna Zicon, Ramky One Galaxia, and My Home Tellapur. The presence of handover-ready towers has also begun fueling organic turnover, where early-phase buyers are now exiting and newer families are entering.

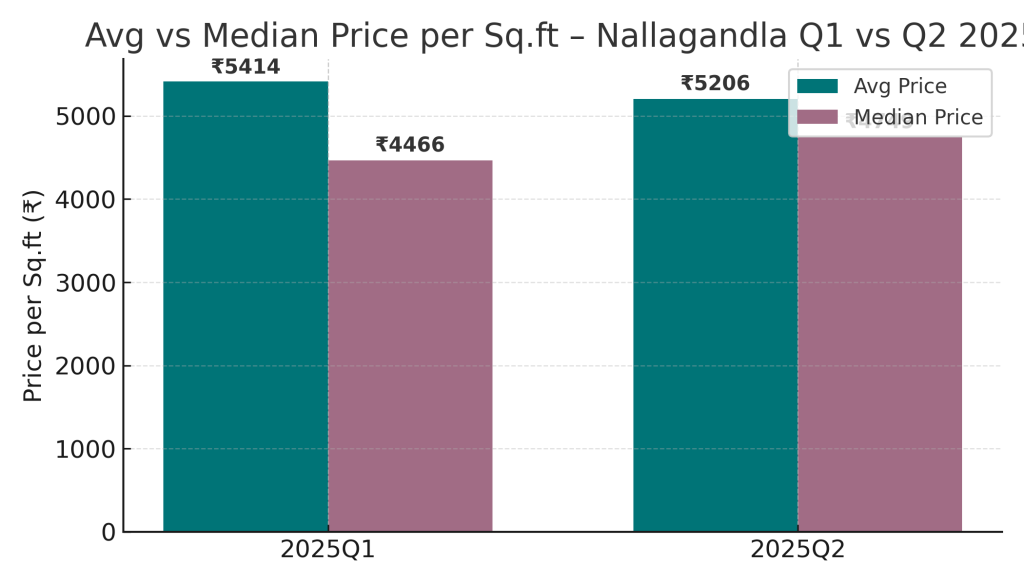

Despite a dip in average price per sq.ft, the median price rose sharply — from ₹4,466 in Q1 to ₹4,749 in Q2. This divergence highlights that buyers are actively transacting in mid-to-premium segments, while older or smaller ticket resale deals are pulling down the mean. The core pricing band around ₹4,700–₹5,000/sq.ft remains intact, reaffirming Nallagandla’s appeal among families seeking gated living with long-term usability.

Key Market Metrics – Q1 vs Q2 2025

| Metric | Q1 2025 | Q2 2025 | Trend & Interpretation |

| Avg. Price / Sq.ft | ₹5,414 | ₹5,206 | 🔽 Decline of ₹208/sq.ft (~3.8%) |

| Median Price / Sq.ft | ₹4,466 | ₹4,749 | 🔼 Rise of ₹283/sq.ft (~6.3%) |

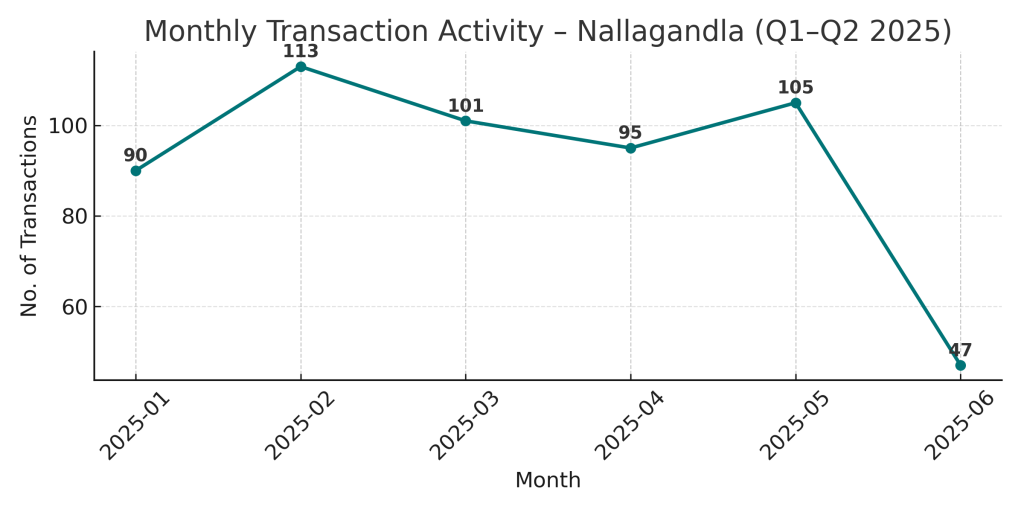

| Total Transactions | 304 | 247 | 🔽 Drop of 57 registrations (~18.7%) |

| Resale Share (%) | 44.7% | 51.8% | 🔼 Noticeable rise in resale activity |

Observations

- Price Realignment, Not Reversal: Average price declined ~3.8%, likely influenced by older or resale inventory entering the mix. Yet the median price climbed 6.3%, showing clear buyer preference for homes around ₹4,700–₹5,000/sq.ft.

- Strong Resale Momentum: Resale share surged from 44.7% to 51.8%, indicating maturing secondary market activity, especially in established gated communities.

- Volume Softening, But Not Weakness: The 18.7% drop in transactions seems more tied to inventory constraints or phased handovers rather than demand slack. End-user absorption remains stable, particularly in the ₹80L–₹1.2 Cr range.

- Nallagandla’s Pricing Band Stabilizes: Despite average price movement, the core pricing zone remains strong and range-bound, reinforcing Nallagandla’s role as a reliable, non-speculative micro-market.

Price Trends & Market Interpretation

Nallagandla’s pricing dynamics in Q2 2025 reveal a balanced and maturing market — one that’s adjusting to supply realities while maintaining steady user demand. The average price per sq.ft dropped slightly from ₹5,414 in Q1 to ₹5,206 in Q2, but this movement is best understood as a realignment toward functional value, not a weakening of demand.

In contrast, the median price rose by over ₹280 per sq.ft, reaching ₹4,749 — indicating that a growing share of transactions occurred in well-specified units within the ₹4,700–₹5,000 band. These are typically mid-to-premium 3 BHKs in gated projects with nearing-possession status, suggesting end-users are driving decision-making based on readiness, liveability, and layout usability.

While average price dips may reflect deals in compact resale inventory or secondary transactions in older blocks, they are not shifting the central gravity of the market. Most developers have held prices steady across towers, often supplementing with possession-linked payment plans or minor financial incentives instead of outright reductions.

Key Signals Emerging:

- Buyers are targeting “value precision” — not the cheapest units, but those that deliver clarity in possession timelines, layout flow, and community infrastructure.

- Median growth signals traction in the mid-premium zone, while outlier resale deals are nudging the average downward.

- There is no price panic — developers are aligned with real-time demand and phasing releases accordingly, maintaining confidence in their pricing strategies.

Resale vs Developer Sales – Market Composition

| Sale Type | Q1 2025 | Q2 2025 | Trend |

| Developer Sale | 168 | 119 | 🔽 Drop in developer sales |

| Resale Sale | 136 | 128 | 🔼 Rise in resale activity |

Interpretation

Q2 2025 marked a clear shift toward the resale market in Nallagandla. While overall transaction volume dipped, the resale segment remained relatively stable, increasing its share of total activity from 44.7% in Q1 to 51.8% in Q2.

Several factors contributed to this trend:

- Maturing community life in earlier phases of projects like Aparna Sarovar Zicon, Ramky One Galaxia, and My Home Tellapur has created a steady pool of secondary supply.

- Buyers looking for quicker possession and transparent pricing found value in resale units, especially those priced between ₹80L and ₹1.1 Cr.

- Many new project launches in the area are either fully sold or between towers, resulting in supply fatigue on the developer side.

In contrast, developer-led sales dropped by nearly 30%, reflecting a more cautious release cycle. Many builders are focusing on clearing backlogged inventory in nearing-possession towers, and holding back new releases until market absorption catches up.

What This Means for Buyers:

- Resale options are increasingly viable, especially in completed or near-completion gated towers.

- Developer inventory may become selective, focused on later phases or premium units.

- For those seeking faster handover, livability, and known community performance, resale may offer better clarity than new launches.

Configuration Distribution – What Are Buyers Choosing?

Exclusive Research. Structured Access.

To preserve quality and purpose,

AIQYA’s research is shared by request.