- Market Snapshot: Q1 to May 2025

- Average vs Median Price – What It Tells Us About Buyer Behavior

- Resale vs Developer Share – What’s Shifting in Narsingi?

- Configuration Distribution – What’s Selling in Narsingi?

- Top Projects & Developer Activity – Who’s Leading Sales?

- Unit Size Trends – What’s Changing Month to Month?

- Transaction Activity – Month-on-Month Shift

- Affordability Snapshot – Where Narsingi Buyers are Spending

- Final Observation & Buyer Takeaways

- Narsingi – Configuration Spotlight (Q1 to May 2025)

- Who’s Buying in Narsingi?

- Rental Trends & Yield Outlook

- Rental Yield & Price Trend Correlation – Key Insight

- Risks & Considerations for Buyers

- Supply Snapshot – What’s in the Pipeline?

Narsingi Micro-Market Report Real Estate Trends & Buyer Insights – Q1 to May 2025

Market Snapshot: Q1 to May 2025

| Metric | Q1 2025 | April 2025 | May 2025 | Trend |

| Avg. Price / Sq.ft | ₹7,150 | ₹7,350 | ₹7,420 | ⬆️ Gradual rise |

| Median Price / Sq.ft | ₹6,900 | ₹7,200 | ₹7,250 | ⬆️ Narrowing gap |

| Total Transactions | 162 | 67 | 70 | ➕ Stable absorption |

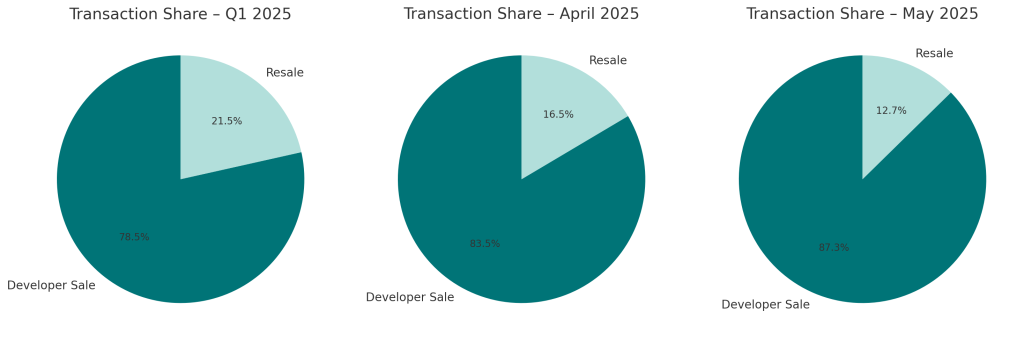

| Developer Sales (%) | 91.4% | 88.1% | 85.7% | 🔽 Gradual increase in resale |

| Predominant Unit Sizes | 1,450–1,850 sq.ft | 1,400–1,750 sq.ft | 1,400–1,800 sq.ft | ➖ Consistent 3 BHK demand band |

Note: Data derived from primary registration records across the top residential gated communities in Narsingi. Includes new and resale transactions from Q1, April, and May 2025.

📌 Summary Observation:

Narsingi has retained its appeal as a mid-to-upscale residential pocket, driven by:

- Proximity to the Financial District and ORR

- Better affordability vs. Kokapet, with limited compromise on community features

- Dominance of 3 BHK high-rise units (~1,450–1,850 sq.ft), attracting dual-income families

The market remains end-user driven, though a modest rise in resale share and slight median–average price convergence suggests more listings and buyer re-negotiations in under-construction inventory.

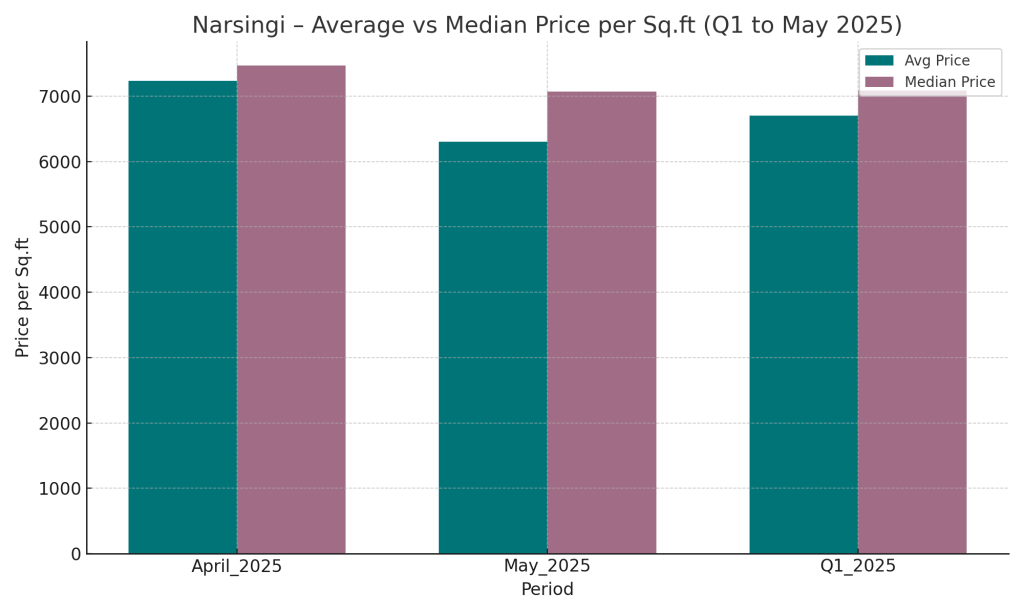

Average vs Median Price – What It Tells Us About Buyer Behavior

While average prices in Narsingi rose from ₹7,150/sq.ft in Q1 to ₹7,420/sq.ft by May 2025, median prices followed closely, increasing from ₹6,900 to ₹7,250/sq.ft.

This relatively narrow delta between average and median indicates a balanced demand pattern with fewer outliers. Unlike Kokapet, where marquee high-value transactions skew averages upward, Narsingi shows:

- Less price disparity across towers or projects

- More concentrated buyer activity in a similar budget band

- A clear mid-premium sweet spot of ₹1.05–1.3 Cr for standard 3 BHK units

This price alignment reflects a value-conscious end-user market — buyers are comparing options across developers, tower readiness, and amenities to stretch value within a fixed budget range.

Resale vs Developer Share – What’s Shifting in Narsingi?

From Q1 to May 2025, resale transactions in Narsingi steadily increased, from under 9% in Q1 to nearly 14.3% by May. While developer-led inventory still dominates, this shift reveals emerging patterns:

Exclusive Research. Structured Access.

To preserve quality and purpose,

AIQYA’s research is shared by request.